The Derivatives Magazine #14

The crypto market continues its gradual rise in the absence of significant negative news. Market sentiment, which is mainly influenced by the anticipation of peak inflation and lower future rate hike ceiling from central banks, is now having the biggest impact on the price movement.

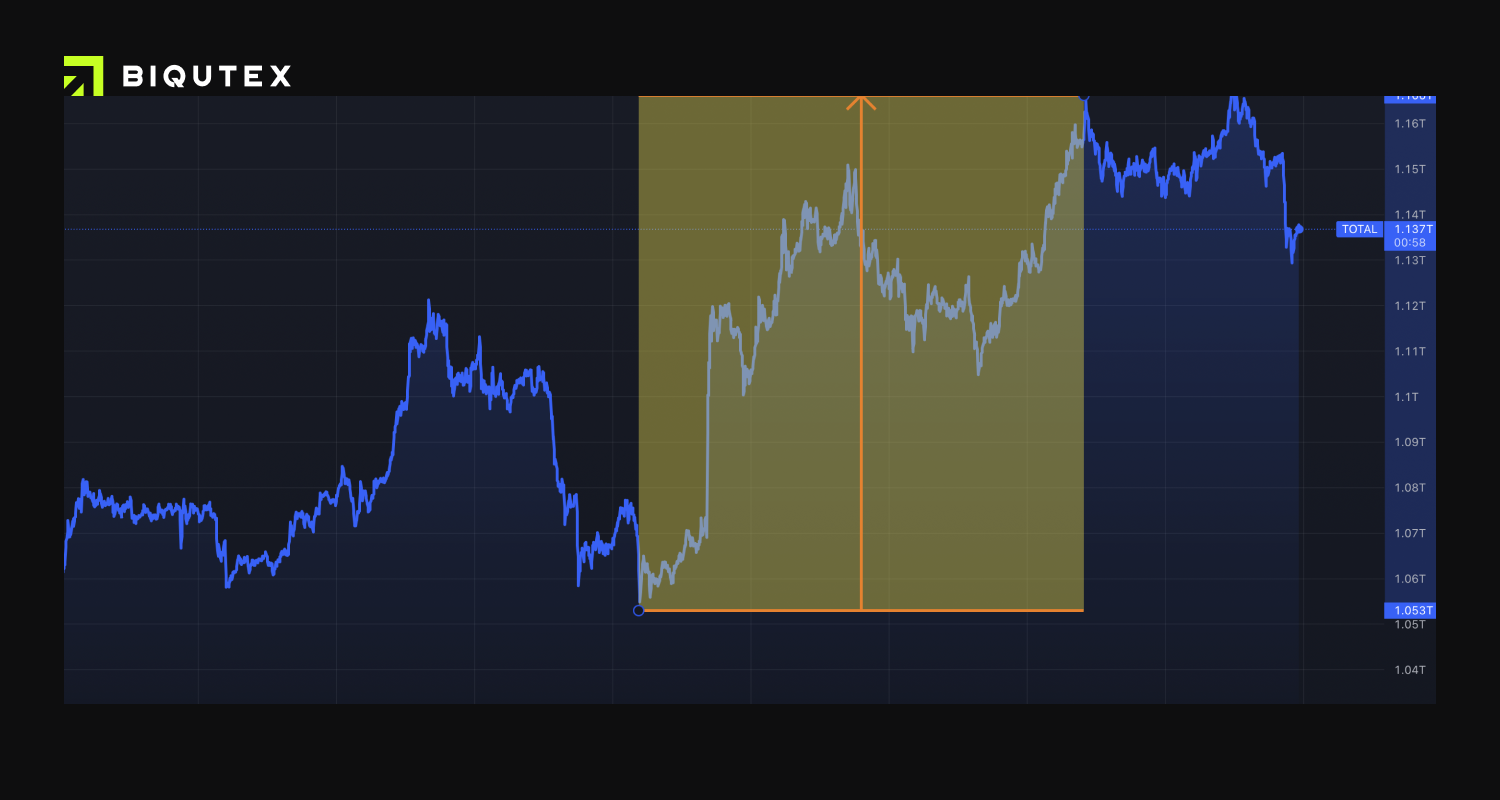

Capitalization growth from the lows of the week was about 10%. Total capitalisation reached $1.11 billion, the highest since the beginning of the summer. Ethereum continues to dominate this growth, reaching the psychologically important USD 2000 mark.

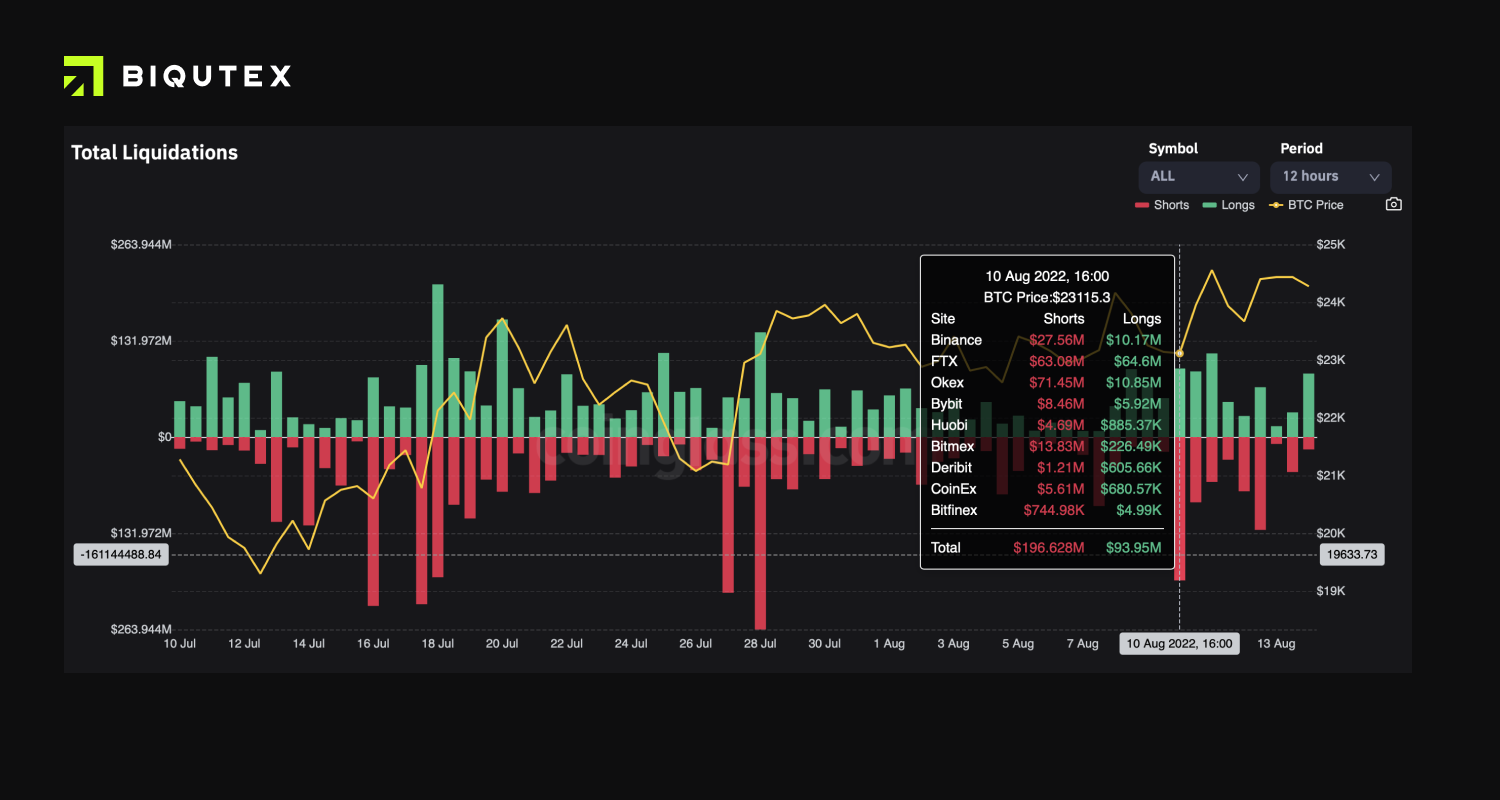

The lack of strong and directional price momentum is leading to an increase in the average liquidation size for both long and short positions. Total liquidations for the week amounted to slightly less than $2 billion, with a roughly equal ratio of short and long positions. Ethereum and Bitcoin have seen the largest amounts of forced liquidations, amounting to 64 million and 46 million respectively over the past 24 hours, according to Сoinglass.

The situation in the funding rate market for Ethereum and Bitcoin continues to differ significantly. While for bitcoin the predominant interest is concentrated in open-ended swaps and long positions, the consistently negative futures rate for ETH is indicative, highlighting the continued demand for the instrument as a hedge to the "merger" process.

Thus, for BTC, the rate range is between -5.95% on the OKEx exchange and +17% on the decentralised DYDX exchange, leaving room for risk-neutral arbitrage.

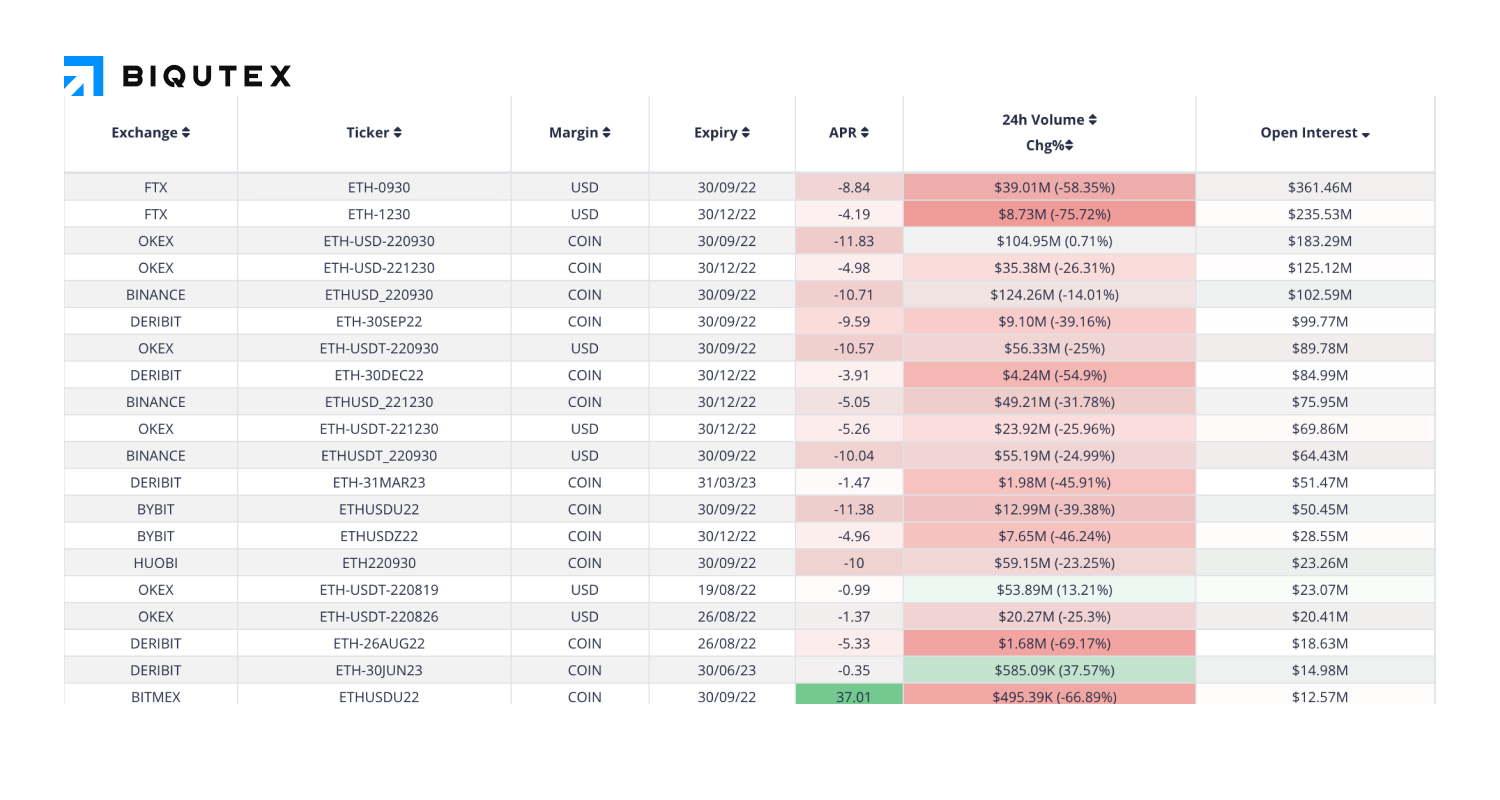

In the case of ETH, funding for the most liquid instruments ranges from -4% for December futures on the FTX exchange to 12% for September exercisable contracts on the OKEx exchange. Overall, September contracts are in the highest demand and the rate on many exchanges is around 10%.

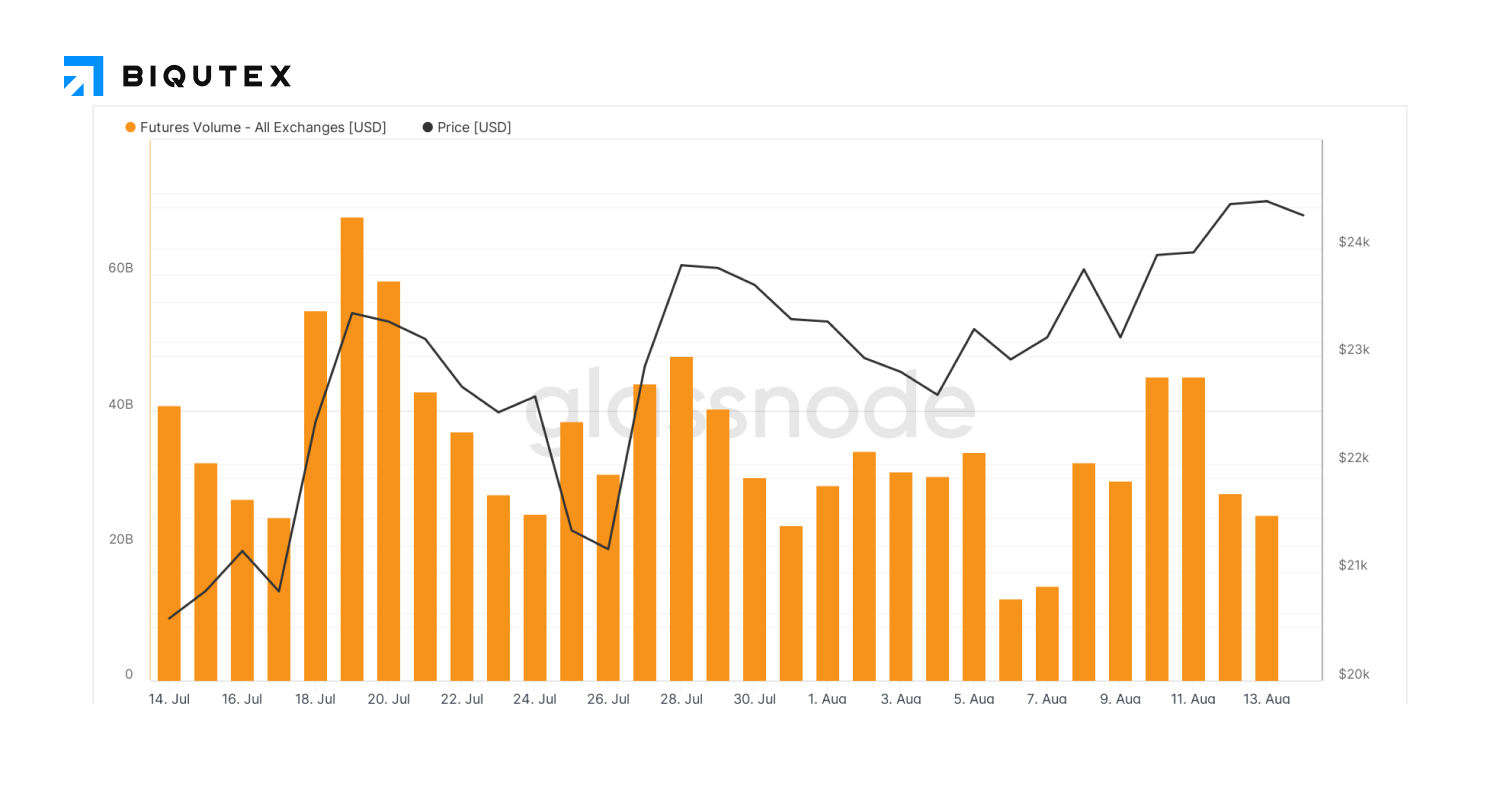

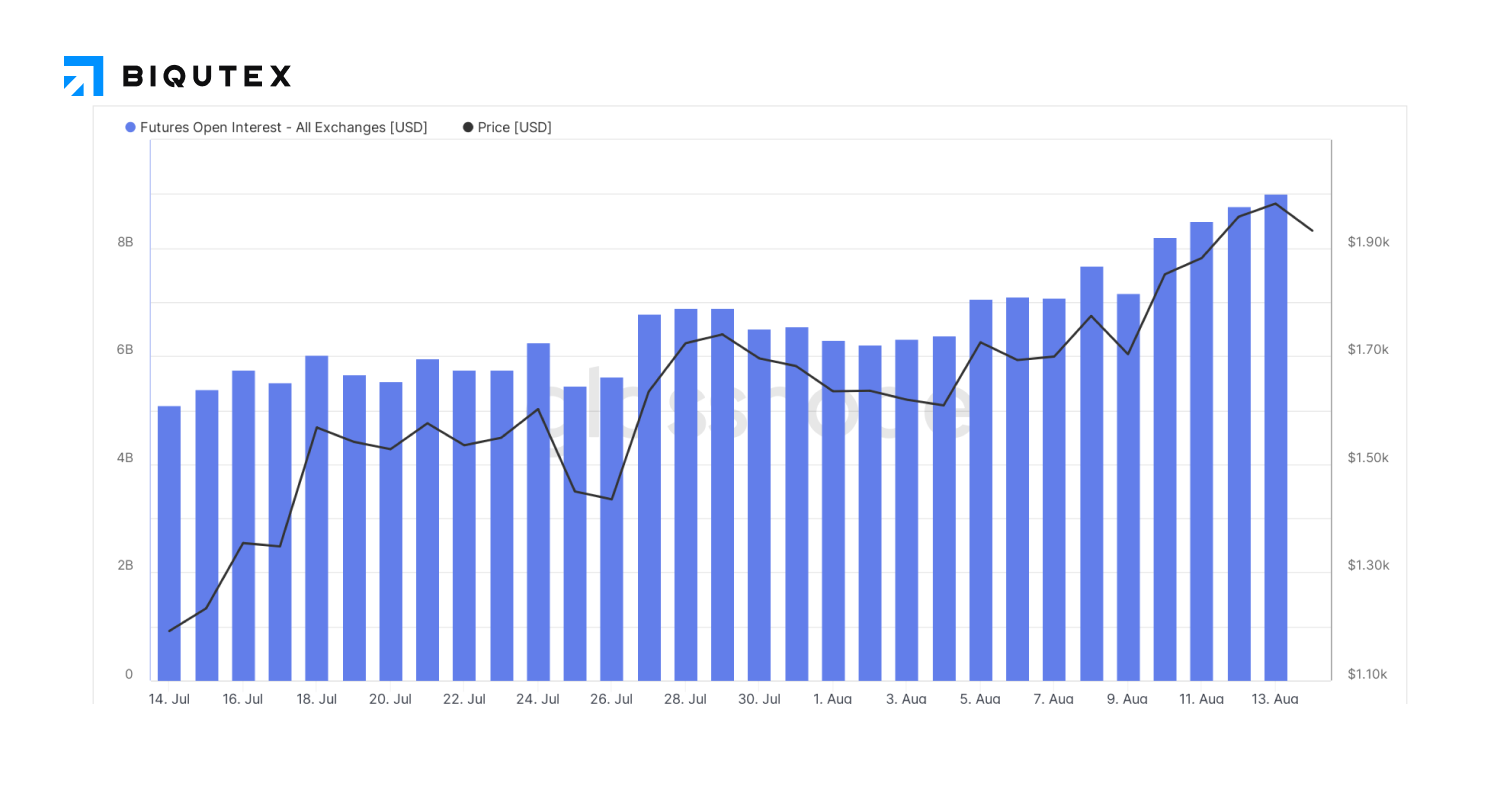

The level of open interest for BTC futures trading remains stable at $12 billion, while trading volume has recovered slightly on the back of spot price increases and is averaging 30 billion daily. So far, there are no large incoming liquidity flows in the BTC market and the market is in a consolidation phase.

For Ethereum, the trading dynamics are more positive. As the spot rate rises, so does the level of open interest, reaching a record high of more than $8 billion. The trading volume is comparable to that of BTC at USD $30 billion per day. This situation in the context of increasing open interest in options (as we mentioned in the last issue) allows us to conclude that the medium-term directional position in the Ethereum market is building up. The dynamics of open interest indicators in this situation is particularly important because it can be used in the future to determine when capital exits the market and possible subsequent trend reversal and price changes.

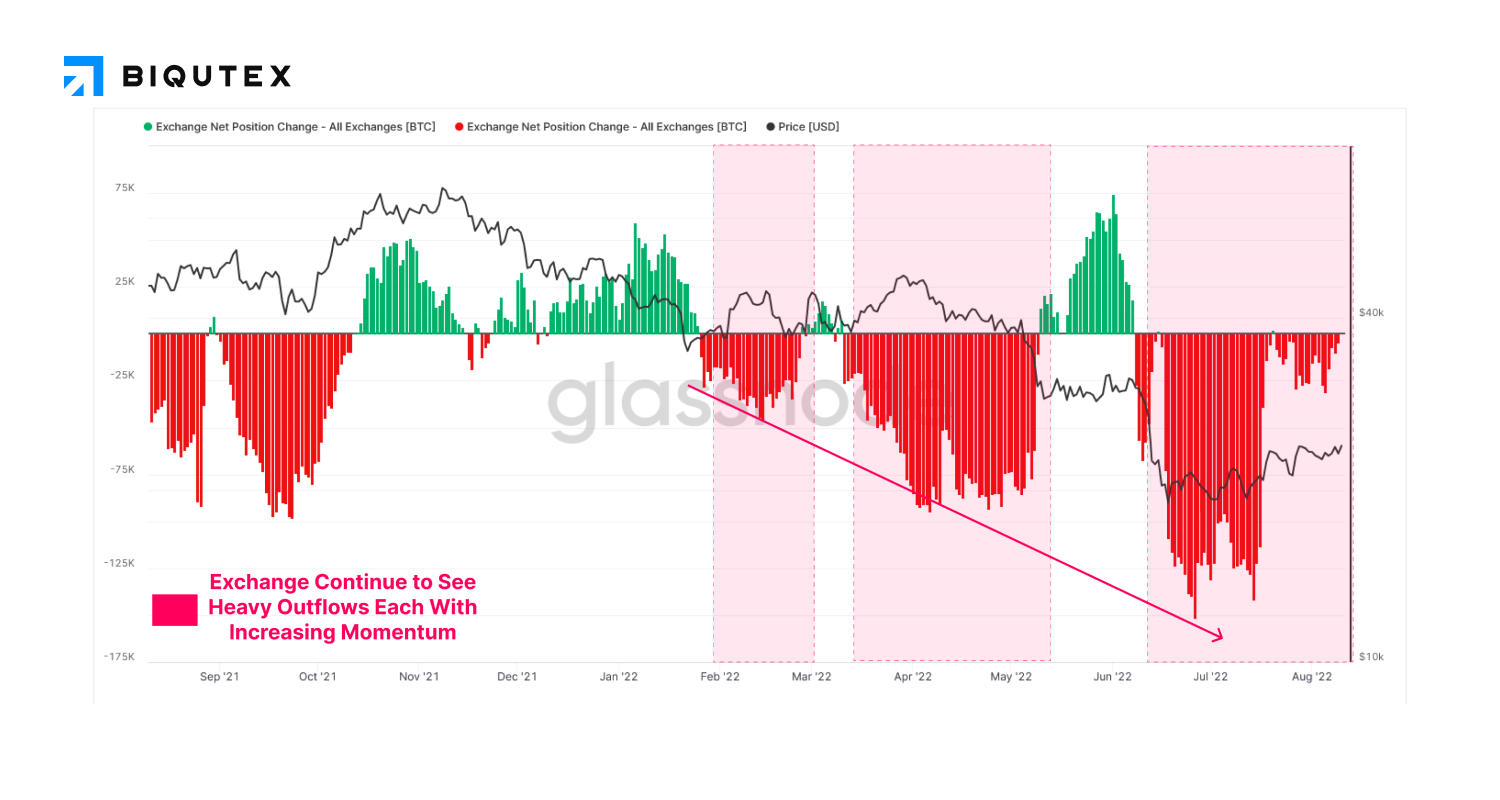

The market situation remains quite complicated. On the one hand, cryptocurrencies are under pressure in the face of negative macro factors. On the other hand, the current price of the underlying assets is at levels that are very attractive for long-term investment. Demand for BTC is supported by the continued momentum of withdrawals from crypto exchanges' wallets. The 20 000 level remains a psychologically important marker for long-term holders to increase their position and new liquidity to enter the market. Capitalisation is also supported by a change in consensus and the formation of a subsequent more profitable ETH token ownership model. Although information on the key aspects of this process (both technical and financial) has long been available, the level of interest from participants is only increasing. In such circumstances, the pause in Fed meetings is good for the market, relieving excessive macro pressure and allowing the market to gain ground on local positive news.

This overview was prepared by the analytics department of the Biqutex crypto derivatives exchange