The Derivatives Magazine #18

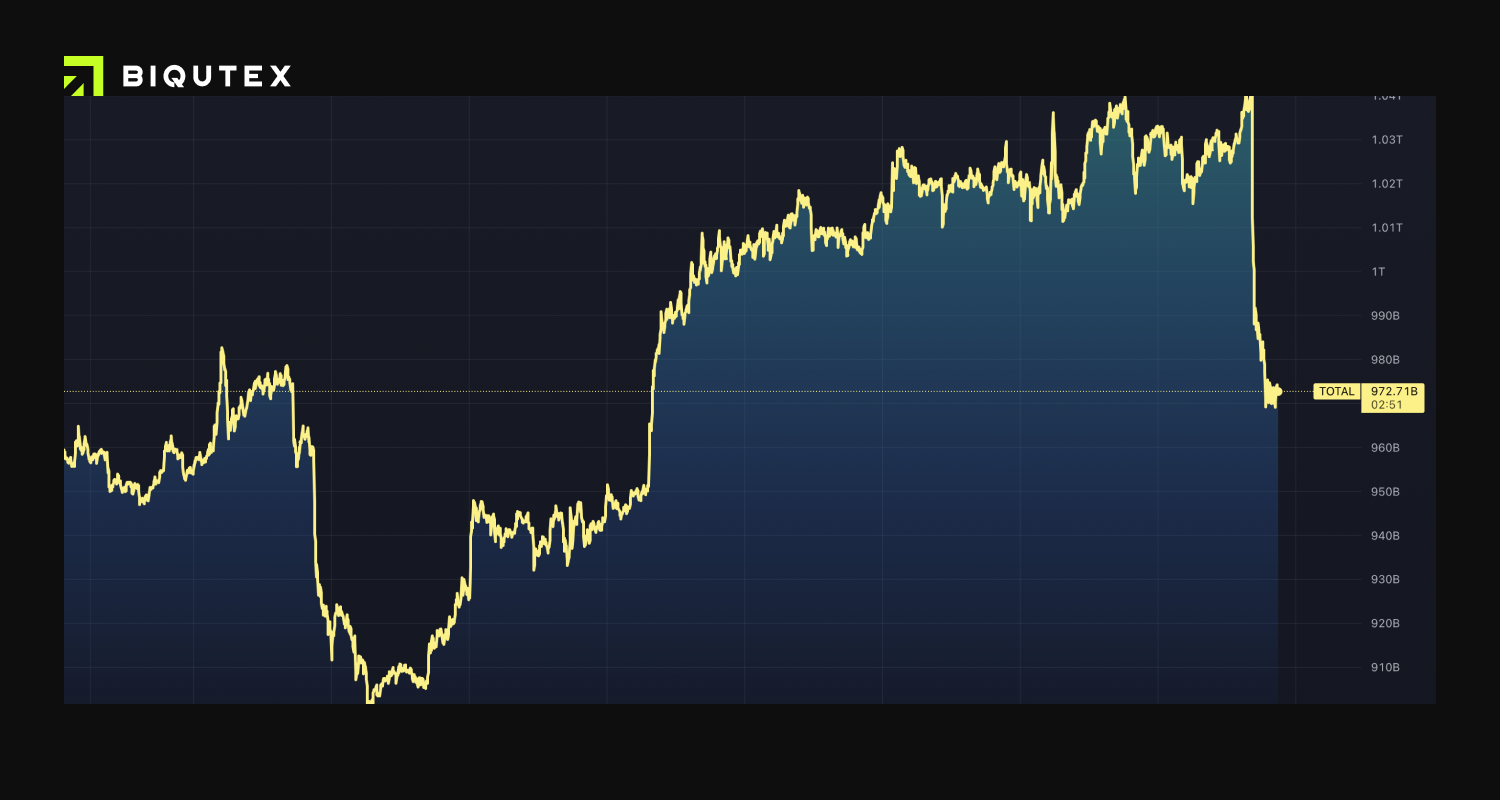

The brief recovery of the crypto market at the end of last week was abruptly interrupted by the release of over-expected US consumer inflation statistics. The final value of 8.3% was higher than most market participants' consensus forecasts and led to a sharp fall in stock indices - SP500 lost 4% in the main session, NASDAQ index 5%. The crypto market was not left behind - total capitalisation fell by 7% to 970 billion.

However, this sharp decline did not result in the significant liquidations that usually occur in such cases. At the time of writing on Wednesday evening, the total amount of forced liquidations had not exceeded USD 190 million, while previous sharp declines have usually resulted in many times that amount. Most of the liquidations were in ETH, amounting to $83 million USD, and BTC, amounting to $68 million USD.

The perpetual futures market reacted to the news with a significant increase in trading volume. The main surge of interest was in ETH contracts, where an increase in short positions and the ensuing imbalance led to an impressive funding rate (more than -100% p.a. on FTX and OKX). At the same time, the rate on BTC contracts, on the contrary, remained in a moderately positive zone (from +10% on Binance to +19% on OKX), providing traders with excellent opportunities for cross currency or spread arbitrage.

Funding rates for September's futures instruments have changed strongly, but less than in the perpetual swap market. The sharp increase in the negative funding rate for ETH contracts was the result of additional hedging of long positions on the spot market. For BTC, the short-term contracts were also mainly used as a cross hedge against surprises under the Fed rate decision at the end of September, and as a way to more price-efficiently cross-hedge on ETH.

The rise in the market and the decline in the price of most crypto assets at the start of the week was accompanied by an increase in derivatives trading volumes. The volume of open interest in BTC has surpassed the 12 billion mark and is trending upwards. For ETH, the fixing of open interest above the 8 billion mark is also a strong indicator - further confirmation of the continued interest in the asset as part of the soon-to-be-updated consensus mechanism.

Onchain data analytics on the Glassnode platform suggest that the current market stage is similar to those at the end of the 2018-2019 bear market. Among the two categories of holders - short-term (up to a quarter) and long-term (from a year) - the behavioural dynamics are significantly different. The 20% fall in the market has led to a slight (2.5%) increase in the number of addresses at a loss for long-term owners and a significant (9.3%) increase for short-term owners. Accordingly, the main additional sell-side activity is currently possible from short-term traders and speculators, while long-term owners continue to buy out drawdowns and keep the asset on balance.

This overview was prepared by the analytics department of the Biqutex crypto derivatives exchange