The Derivatives Magazine #22

For the fourth week in a row, the cryptocurrency market is in a period of low volatility. Despite the unfavorable condition of the world markets (increasing rates of the world central banks, "strong" US dollar, anti-record stock prices of the leading world banks, etc.), bitcoin looks quite stable, keeping the cryptocurrency market relatively sustainable in comparison with other markets. During the past week, the total capitalization index moved within the range of $885-935 billion, ending the week at $904.5 billion.

The volume of liquidations decreased in absolute terms compared to the previous week, which can be clearly seen in the above chart. The big proportional difference between liquidated long and short positions (in favor of short ones during the growth and long ones during the fall) indicates that the uncertainty is still very high. For this reason, market liquidity continues to remain at minimum values.

For BTC futures contracts with an expiration date in late December, the funding rates continue to remain around zero (with a slightly higher percentage on Binance), suggesting that traders are not motivated to increase risks in the current environment. Also, the second highest volume of open interest (despite a daily drop in trading volume of 16.43%) is a contract on the OKX exchange with an expiration date in late March (also with a near-zero rate).

The small negative funding rates for ETH futures contracts (from -1.77 to -3.40%) suggest that traders' expectations are slightly skewed toward the asset's decline.

Bitcoin open-ended swaps show much higher interest rates. Most of the contracts with the highest level of open interest are in the positive zone (except for the contract on the FTX exchange with a rate of -2.63%). This indicates relatively consolidated expectations of traders.

In the case of Ether the rates are also higher than the futures contracts, but most rates (except for one type of contract on the Binance exchange with a rate of 3.89%) are in the negative zone. In this case, if we consider the average rate for 7 days, the traders' expectations are contradictory.

An interesting fact is a sharp increase in trading volume for all contracts (from 15.36% to 48.94% in 24 hours). This, in its turn, is a growth indicator of short-term speculative activity, caused by expectation of the US economic data publication this coming Thursday.

Over the past week, about 65k ETH and about 19k BTC were withdrawn from exchanges in total. Market participants are slowly accumulating their positions, as a consensus is forming among analysts regarding the formation of the supposed "bottom" of the crypto market (at least judging by the on-chain data).

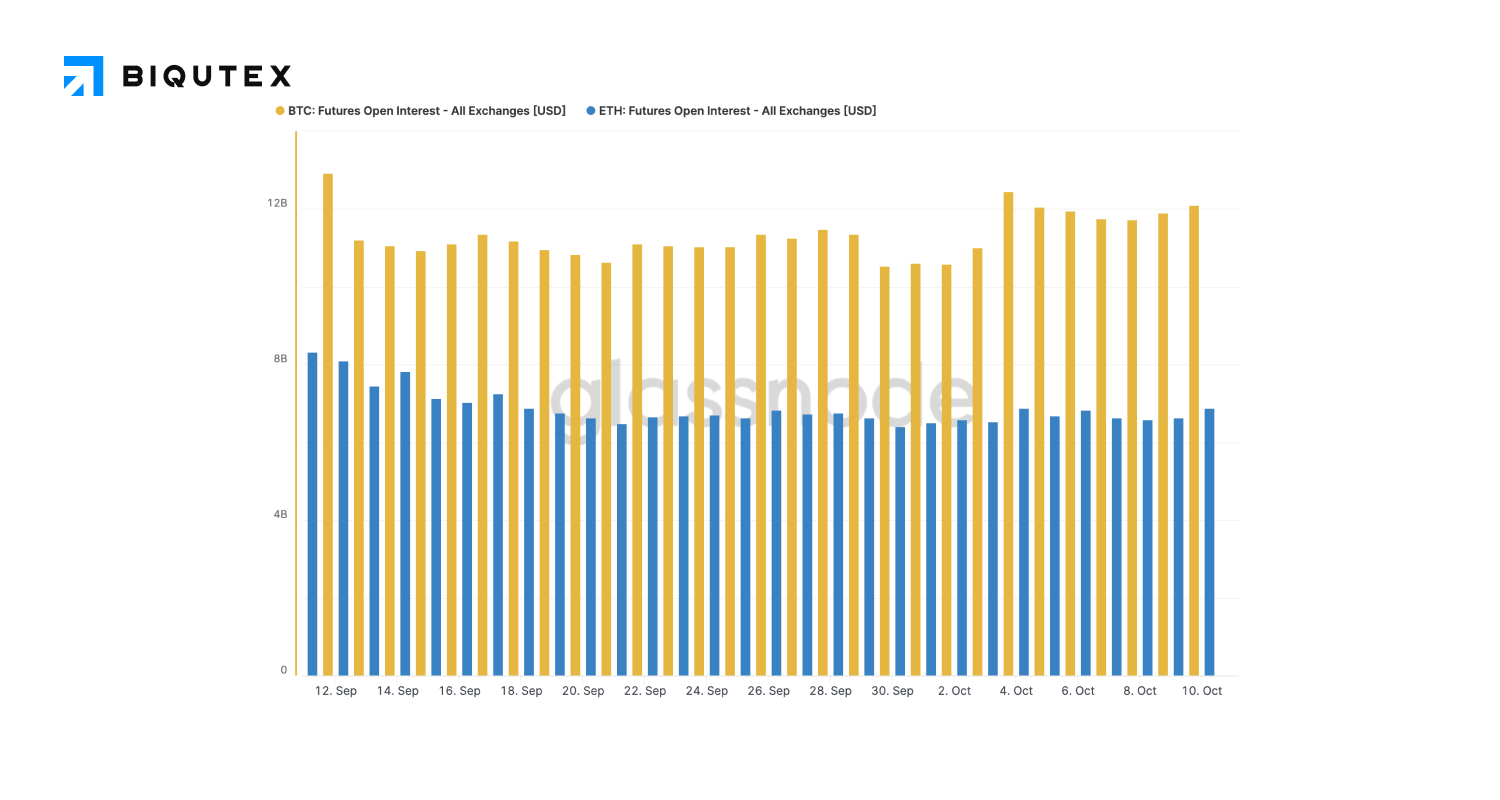

The level of open interest on BTC futures contracts was slightly higher than during the previous few weeks. Open interest on ETH futures actually did not change. Given the low liquidity and market consolidation, this indicator is rather uninformative.

The five-day activity pattern in the futures market (which can be explained by the high proportion of institutional investors who tend not to trade on weekends) has once again been confirmed this week. Nevertheless, the volume of weekday trading declined for the second week in a row, which points to a general decline in activity.

According to Glassnode analytics service, as of October 8, the realized value of bitcoin from short-term holders (STH-RP) was below the realized value of bitcoin from long-term holders (LTH-RP) for 15 days (17 days as of October 10). This is a much shorter period of time than during the bear market of 2014-2015 and 2018-2019. During previous cycles, the return of STH-RP to positions above LTH-RP coincided with the start of a new market growth phase, hence it suggests (but does not guarantee) that the same should be expected within the current cycle. However, it remains an open question how long will this period last (judging by the length of the previous ones, we have to wait at least a few more months before the market starts to recover). We should also not ignore macroeconomic factors and tensions in international relations, which can make adjustments to the market recovery timeframe.

This overview was prepared by the analytics department of the Biqutex crypto derivatives exchange