The Derivatives Magazine #10

The 10th anniversary edition of The Derivatives Magazine comes at a most favorable time compared to previous editions. Over the past week, the crypto market capitalisation has risen by around 20% to more than $1 trillion. The main growth driver was ETH, which gained about 40% over the weekend and pulled all other tokens with it, reaching the price of more than $1500.

The surge was linked to several large trades on the spot and options markets, when the use of the Covered Call strategy forced MM to also increase the underlying asset (ETH) stock on balance sheets, which also helped to push the price up.

Such a sharp move could not help but affect the level of liquidations in the markets. According to Coinglass, liquidations increased significantly on Saturday and Sunday, amounting to around 600 million over the weekend. Ethereum accounted for the bulk of the expected share, amounting to 233 million (including Monday’s over 320 million), triple the level for Bitcoin. Despite the fact that ETH growth was strong and quite rapid, long position liquidations account for around 40% of total volume.

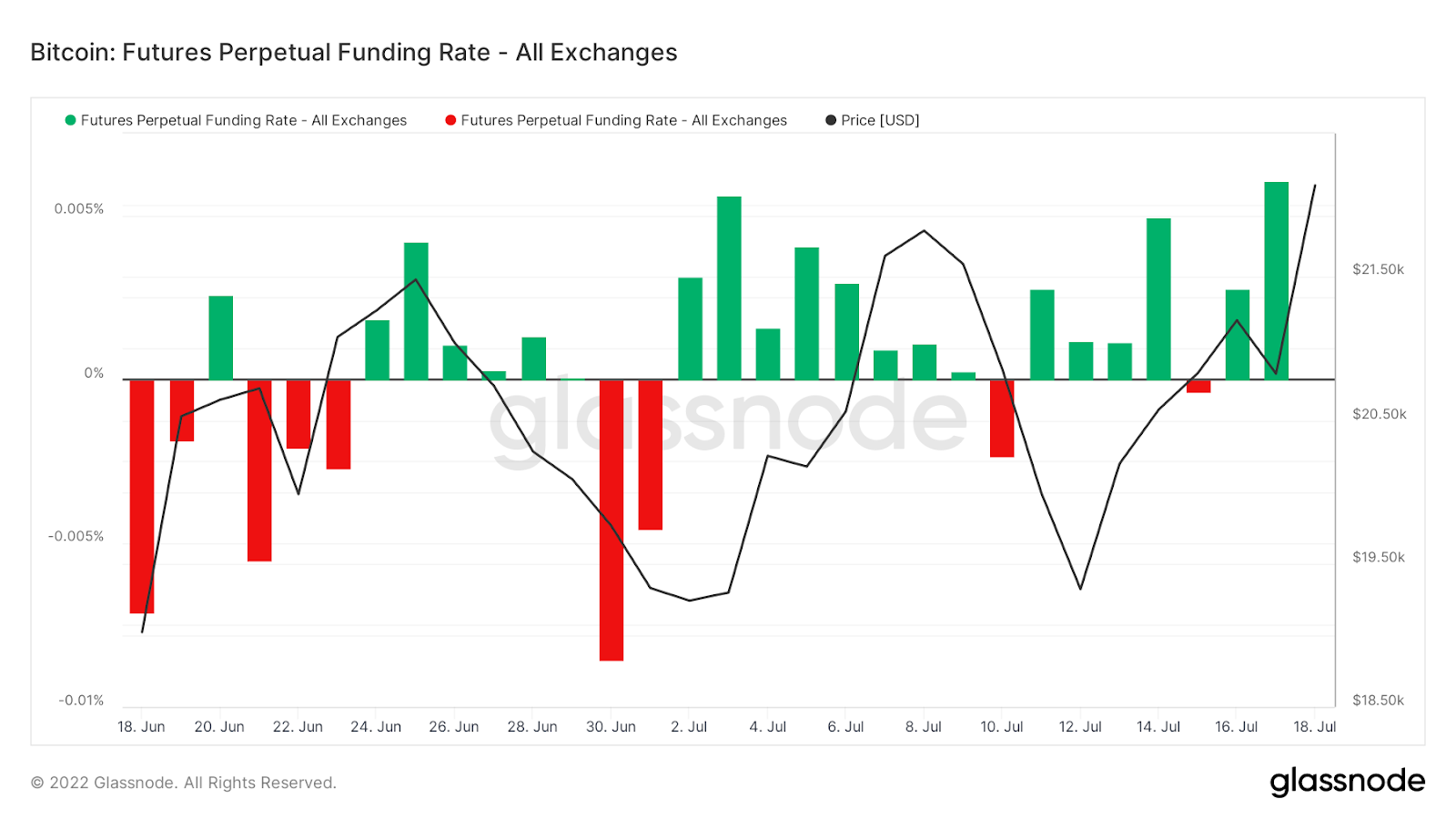

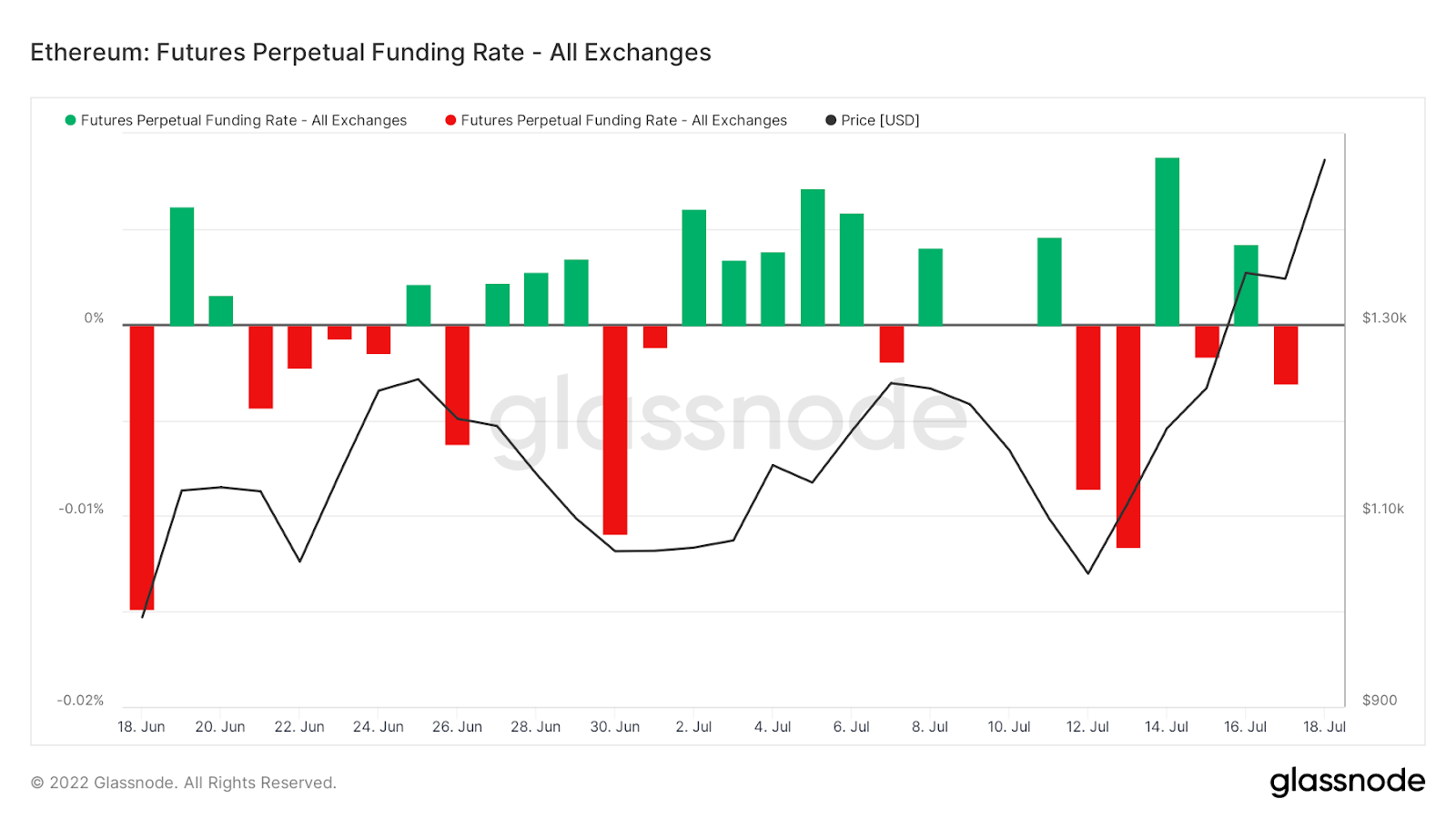

Perpetual swaps continue to be very popular among traders. The funding rate has increased on most exchanges and averages around 10% p.a. regardless of the collateral type (token or staple). On several exchanges (DYDX and OKEX), the rate increased significantly along with open interest in the instruments and exceeded 14%, indicating an increased and consolidated demand for leverage to maximise the current result as long as market conditions allow.

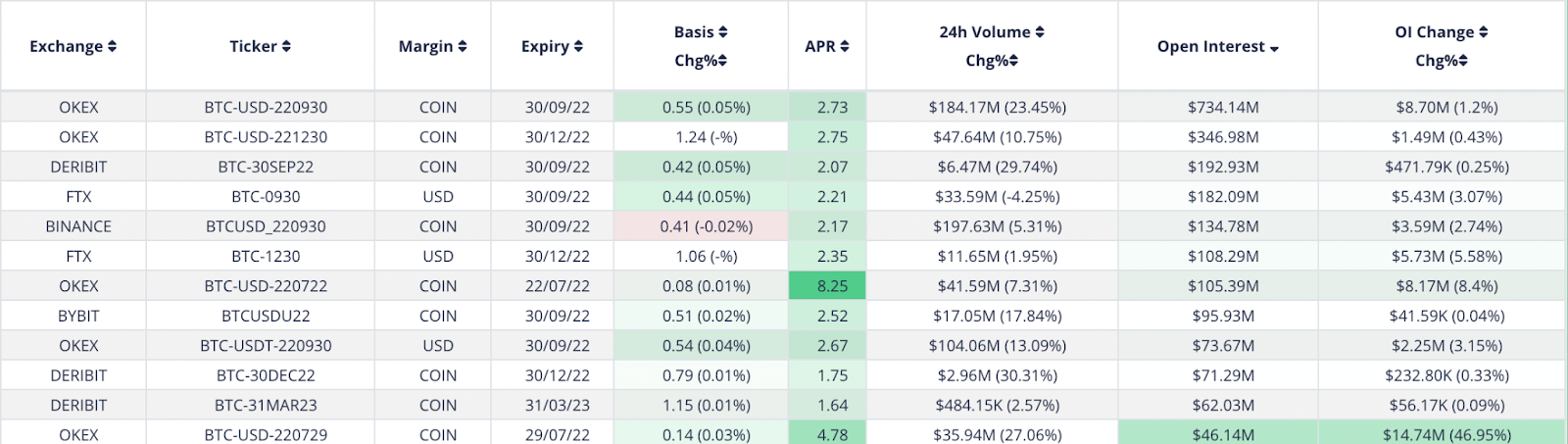

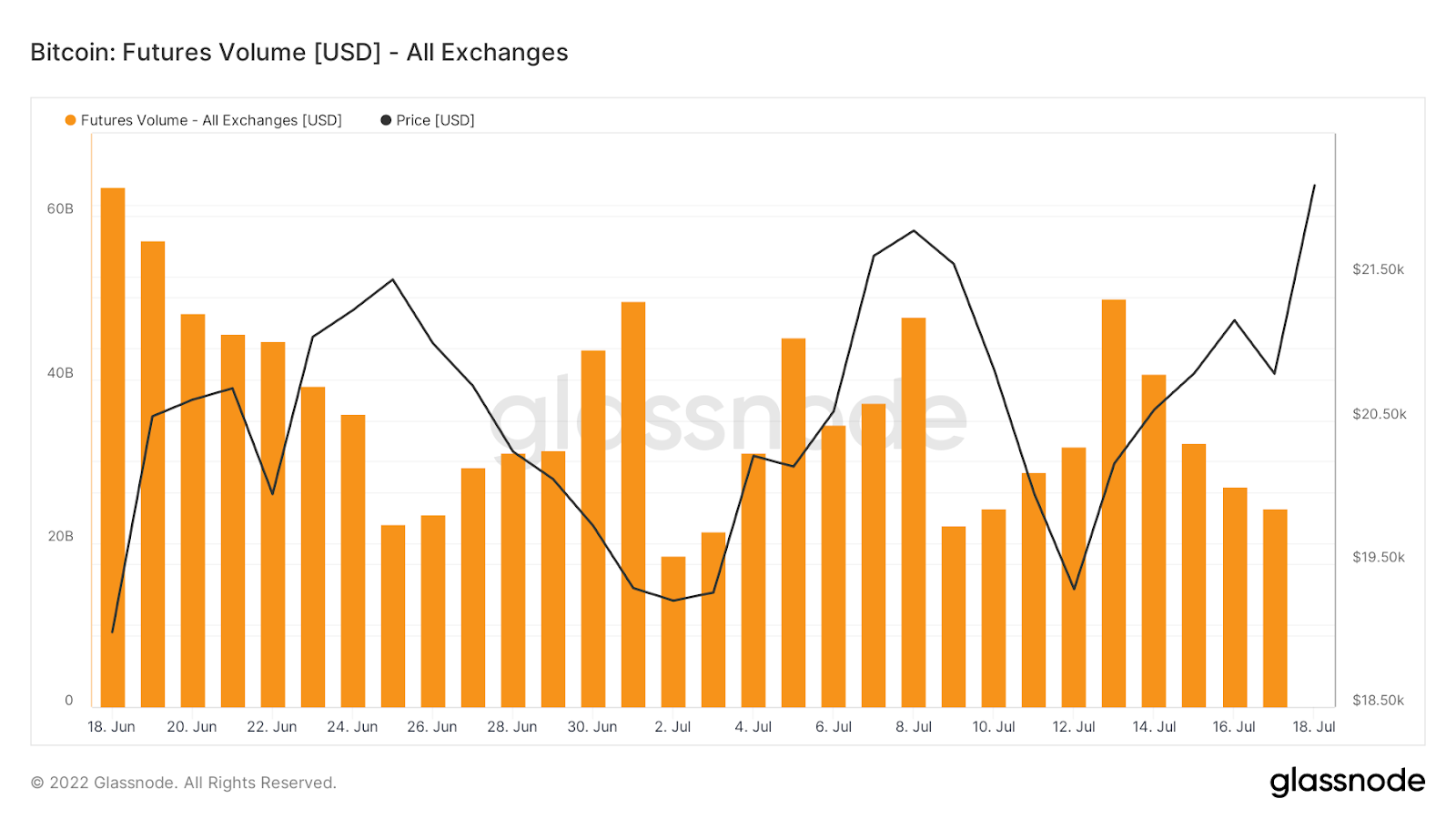

In the futures market, the bulk of the volume is still concentrated in September-dated instruments. The funding rate is not very high except for Deribit, where there has been a surge in trading volume (and thus the rate) for September and December contracts, due to active options trading on the exchange.

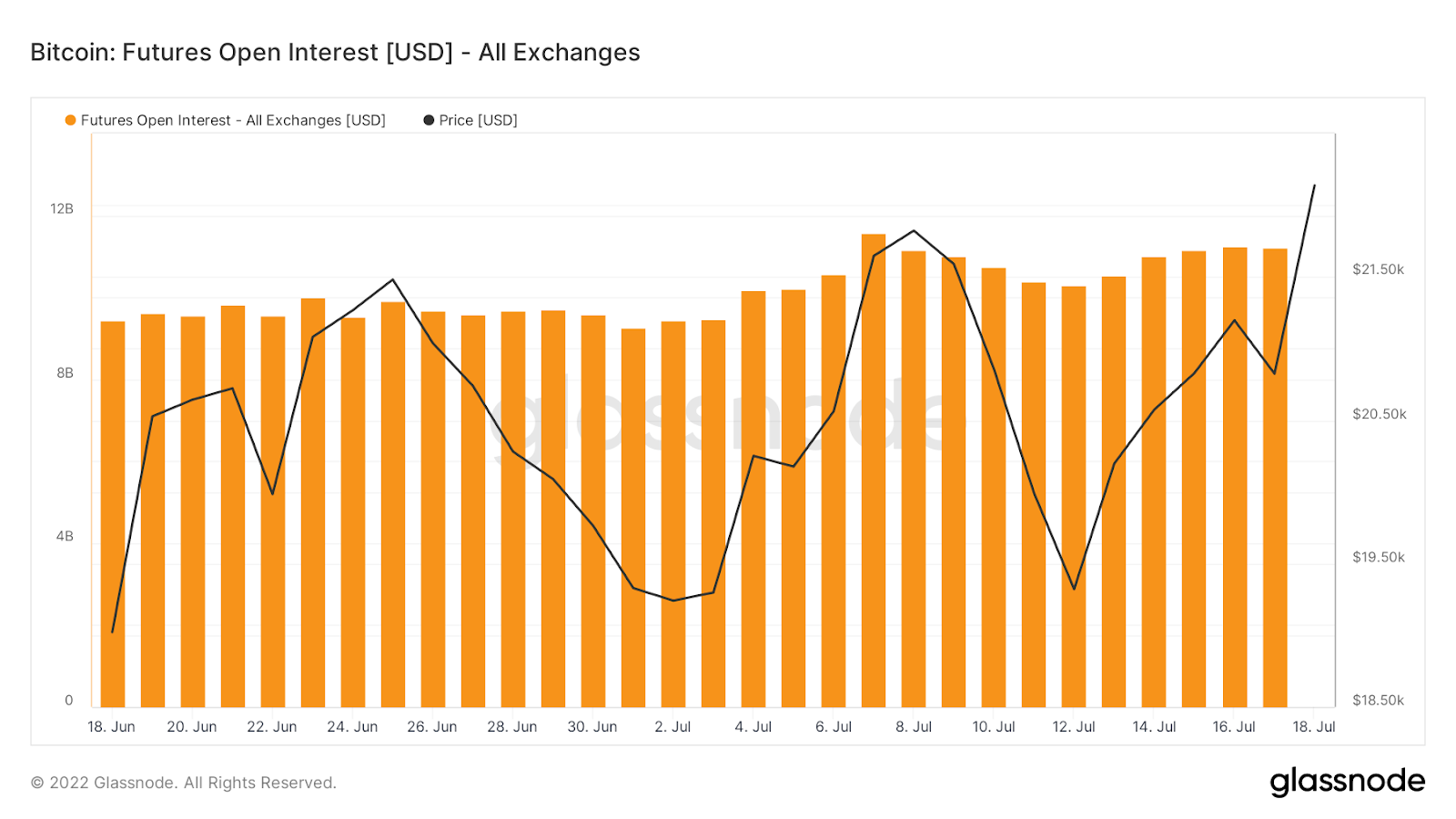

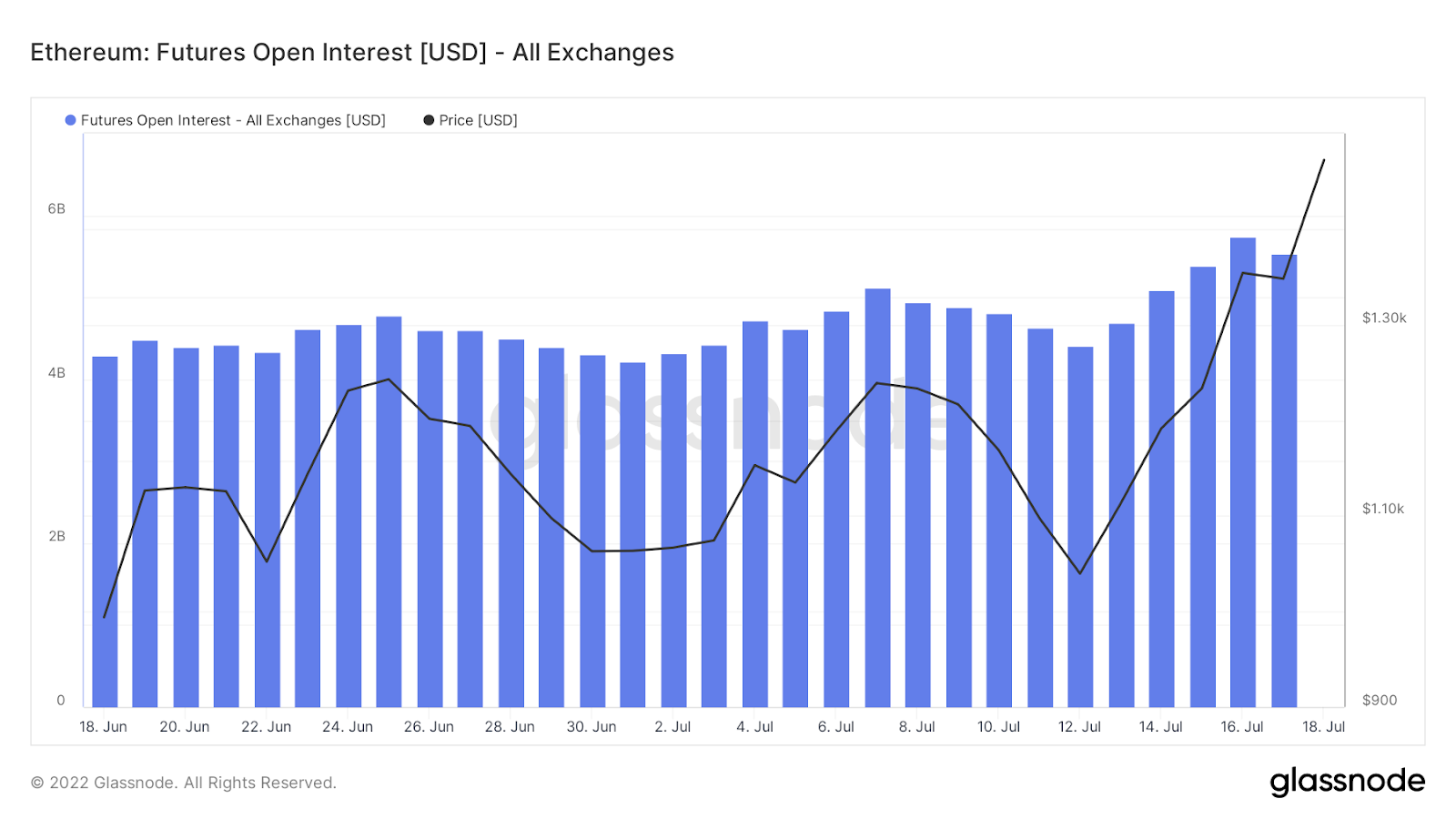

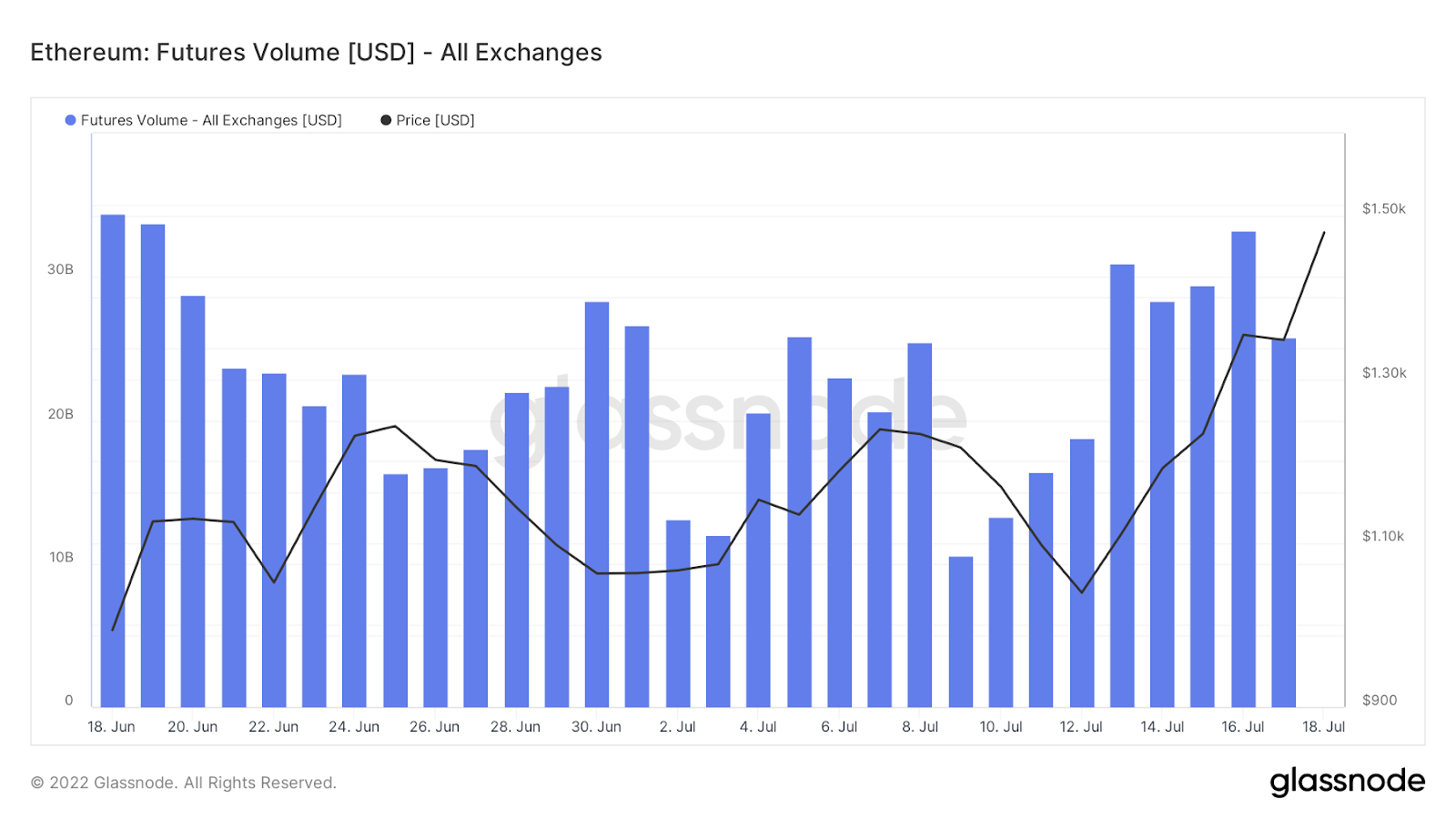

Bitcoin’s open interest volume has remained stable, despite a slight decline in trading volume over the past few days. The correlation between rate increases and trading volumes is due to the fact that unlike past historical periods, when Bitcoin was the first to respond to softening market conditions, in this situation the Ethereum token was leading the way.

The differences in trading volume and open interest dynamics between Ethereum and Bitcoin are more noticeable when compared across funding rates and price movements. Despite the small increase in figures, the rise in the value of ETH was much more significant, reflecting the limited number of participants and capital involved in the growth.

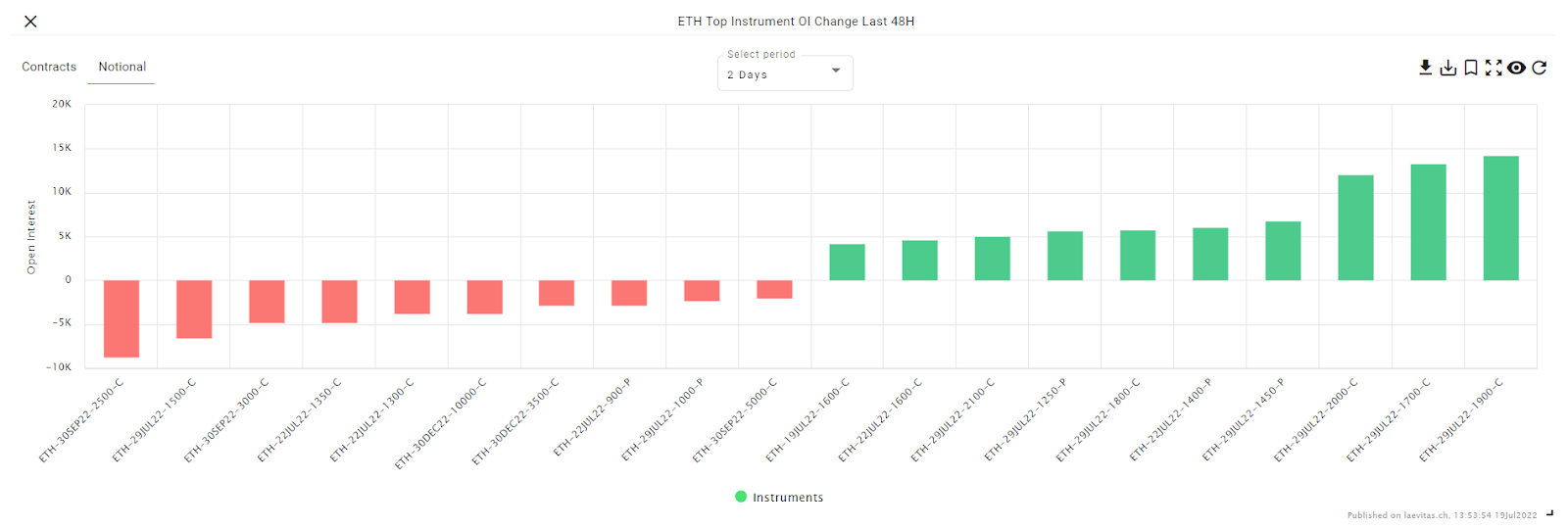

The CALL options trading map for ETH shows a sharp increase in interest and trading volume for individual instruments – such as the 1 200/1 400/1 700/1 900 levels and the late July and late September expiration dates. Of course, the main growth driver is MERGE and the consensus shift is as important as, if not better than, the halving process in Bitcoin. However, the news of the upcoming event was known quite in advance: the first reports of the successful tests had appeared a month earlier, giving investors plenty of time to accumulate capital. The timing of options transactions – weekends, when there is very little liquidity in the market – indicates a deliberately chosen and prepared way of entering the market and may be aimed at gaining not only long term profits but also short term ones, within the framework of options trading. In any case, regardless of the planning horizon, this is a positive development for the market. Many participants took advantage of the situation to buy on an oversold market. The strength and duration of this trend will largely depend on the central bank news next week and the behavior of the stock market indices. In the absence of significant negative news, prices of major cryptocurrencies may consolidate at the levels reached.

This overview was prepared by the analytics department of the Biqutex crypto derivatives exchange