The Derivatives Magazine #12

The overall capitalisation of the crypto market continued to rise last week. Having gained around 8% and finally consolidated above $1 trillion, the cryptocurrency sector is showing positive momentum and is one of the main beneficiaries of the global market’s consolidation phase. The fashion of the past two months for sharp price movements over the weekend has paused this time, indicating a relative stabilisation of the market and the end of the forced (and sudden) liquidations and related speculation.

The recovery in prices for a wide range of crypto assets has led to a significant level of short position liquidations. In the past week, it amounted to around $1 billion, while for long positions it did not exceed 500 million. According to the coin glass analytical service, Ethereum remains the main asset for margin trading, more than twice surpassing Bitcoin in terms of volume of forcibly closed trades.

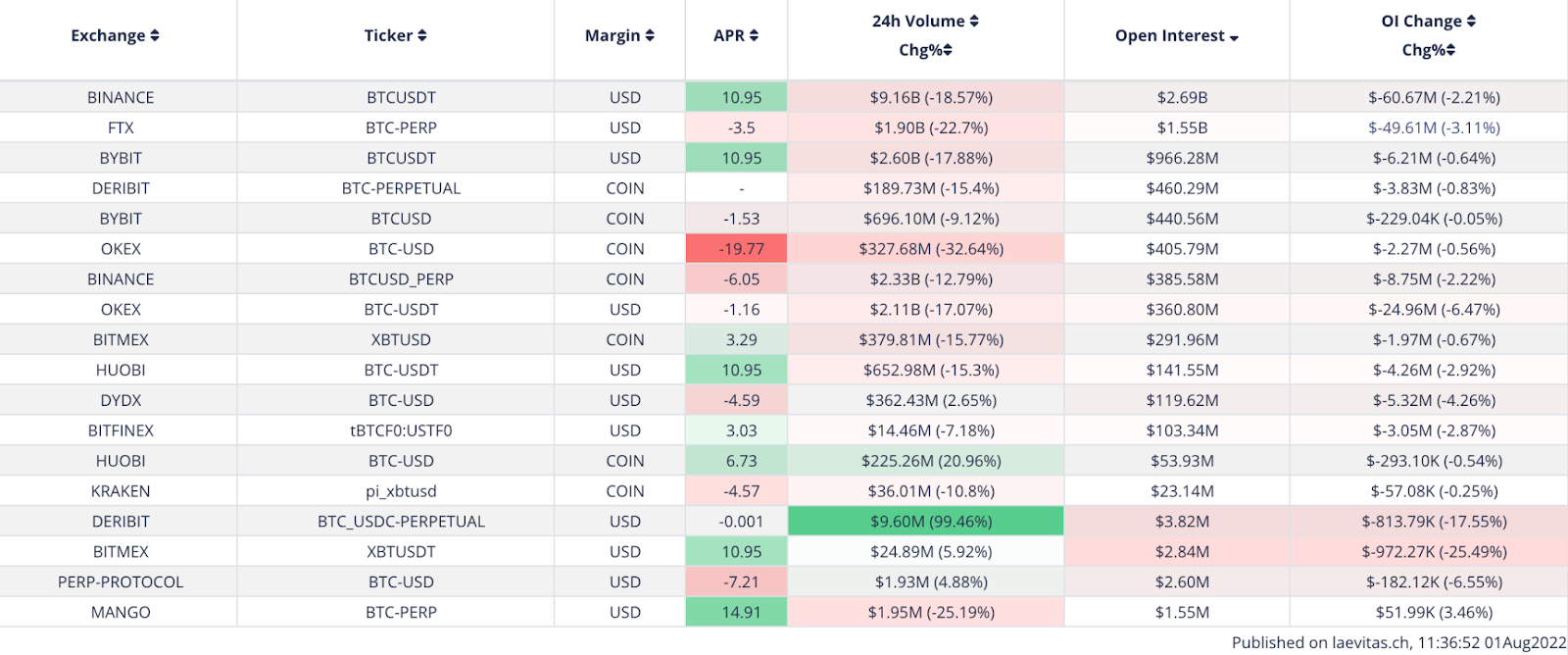

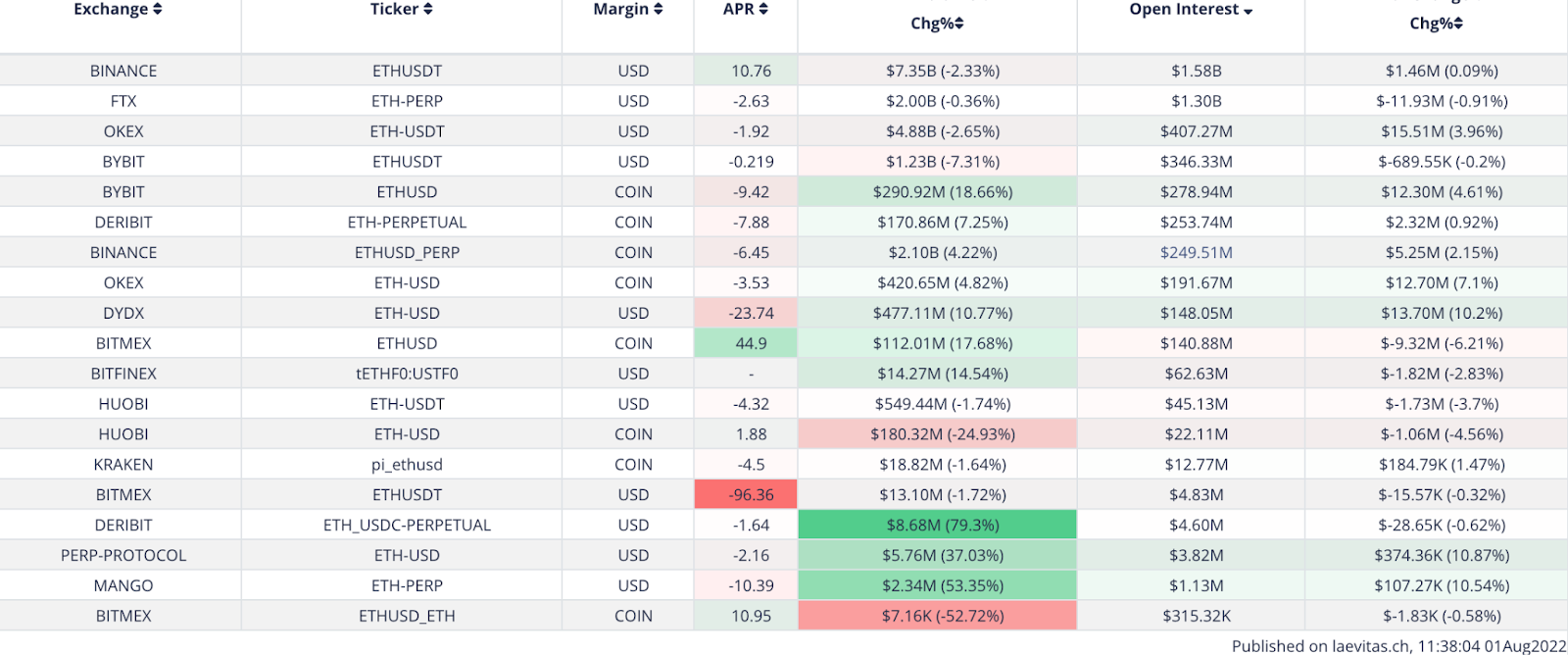

The trading process for open-ended futures is dynamic and fragmented. The funding rate for some venues in the top 10 by volume is as high as 20%, while on exchanges with maximum liquidity (Binance, Bybit) it is at least 10% APY.

The level of open interest rose slightly and consolidated above the $12 billion mark. While the rise in the spot price has been accompanied by a decline in trading volume, this could be one of the drivers for further growth, especially when traders’ attention shifts away from the ETH network update. Historically, the trading volume figure directly correlates with the price growth, and the difference in dynamics at the moment could indicate either a weak price growth foundation and an imminent reversal or a price lag and further growth to the 27 000-30 000 mark.

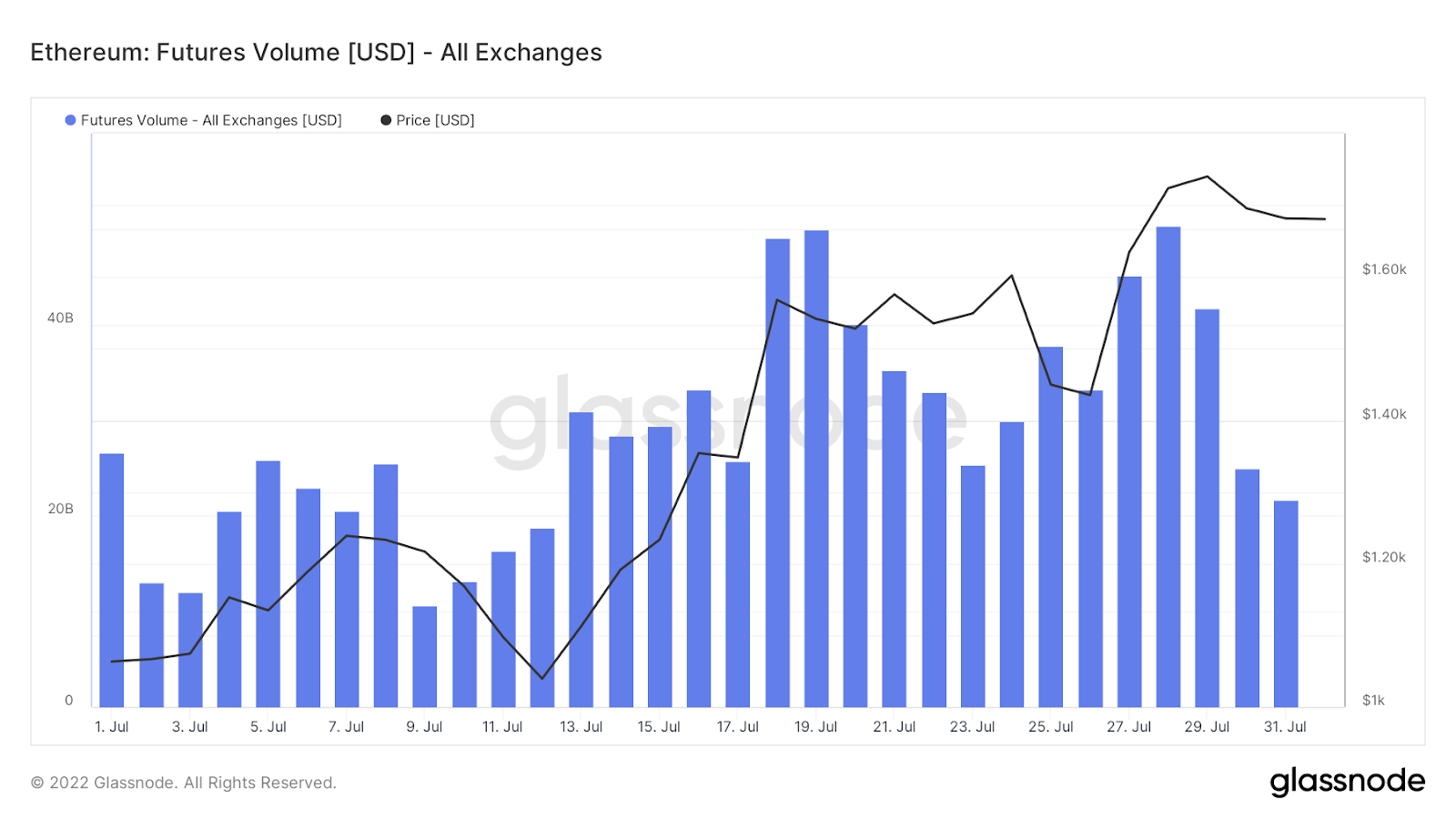

For Ethereum, trading volume figures of up to 40 billion and sustained open interest above the 6 billion mark are directly in line with the price increase. ETH will continue to see higher demand until the end of the month, as the closer the update with the consensus shift, the more data is emerging on the future yield of token ownership. According to Сoinbase analytical department, the potential passive yield could be around 10% annually, making ETH one of the most profitable POS tokens on the crypto market.

The options market confirms observations about Ethereum’s dominant role in the current (and possibly future) price growth cycle. The Put/Call options ratio is near the 0.25 mark (4 Call contracts for every Put contract traded). The indicator has been changing rapidly over the past three months, in line with the subsequent news about the successful completion of the ETH testnet. In comparison, for bitcoin the figure is 0.45, and has barely changed since the beginning of May.

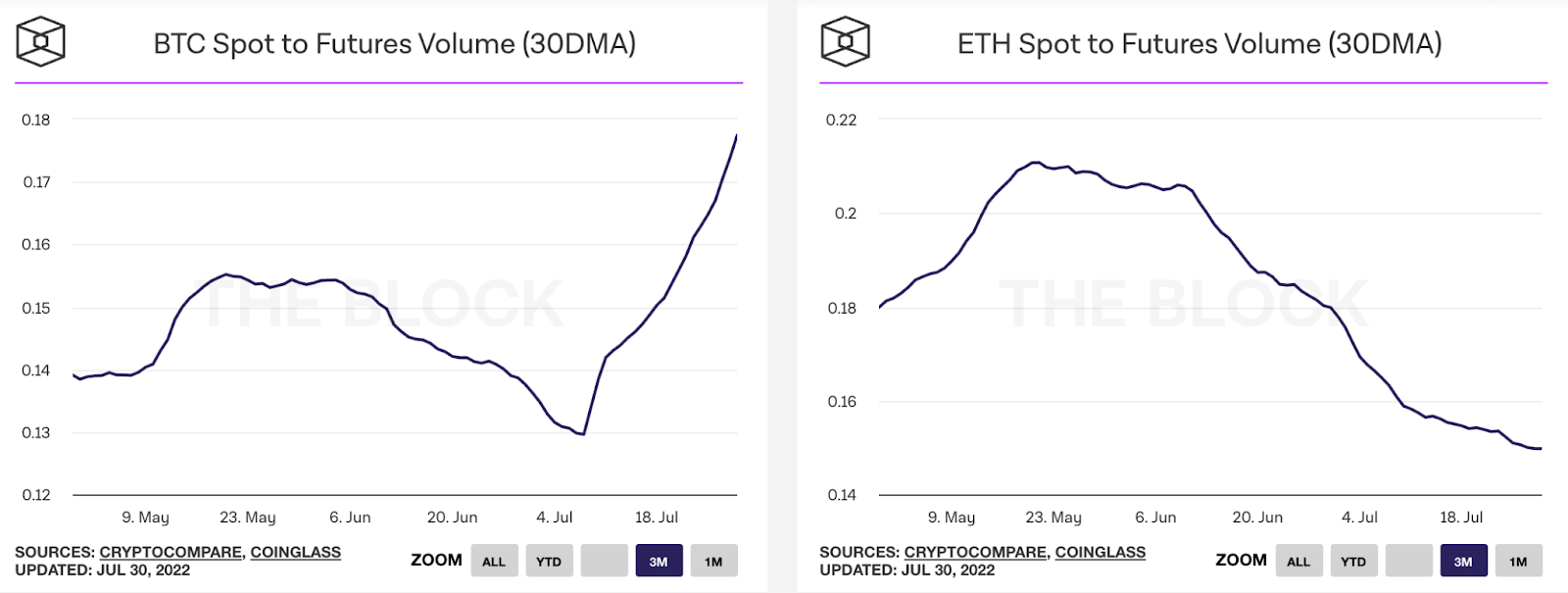

The difference between ETH and BTC is even more evident from futures trading dynamics perspective. Since early July, derivatives have taken an increasing share of crypto asset trading. Crypto trading is becoming increasingly similar in structure to traditional markets, where futures and options significantly dominate volume over spot trading. ETH futures are trading 30% higher than they did at the beginning of the month, while the opposite is true for BTC, where spot trading is up 25%.

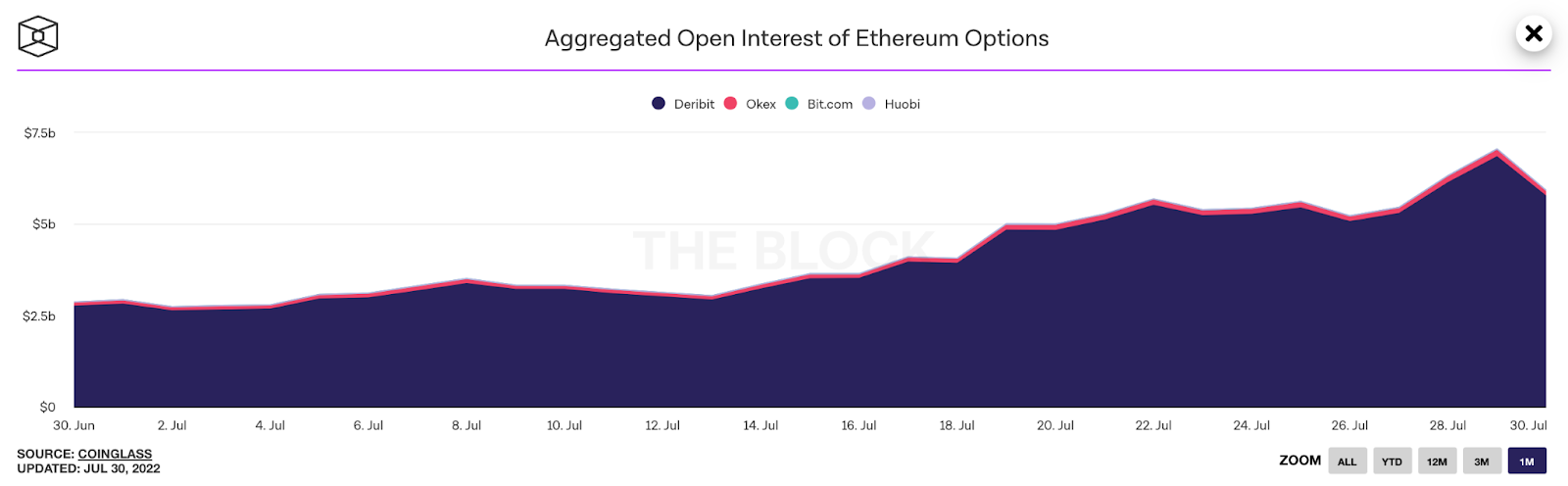

In addition, we note the increased level of open interest in ETH options. Despite the cyclical nature of options trading (at the end of each week/month and quarter, the corresponding volume is settled and written off), the figure has reached over 5 billion, more than doubling in three months. Again, the same figure for BTC is almost unchanged during this time, with an increase of up to 10%.

This set of statistics strongly suggests that if there is any near-term growth in markets, it is Ethereum, and the entire associated ecosystem, that will have the strongest effect on the crypto market.

This overview was prepared by the analytics department of the Biqutex crypto derivatives exchange