The Derivatives Magazine #13

Last week, total crypto market capitalization was almost unchanged, staying in a narrow range of USD 1 to 1.08 trillion. With no significant changes in macroeconomic background and local growth drivers exhausted, traders are looking for new drivers to form a directional move. It is likely that a strong reason for price direction will be the CPI statistics for the US market, which will be released on Wednesday, 10 August.

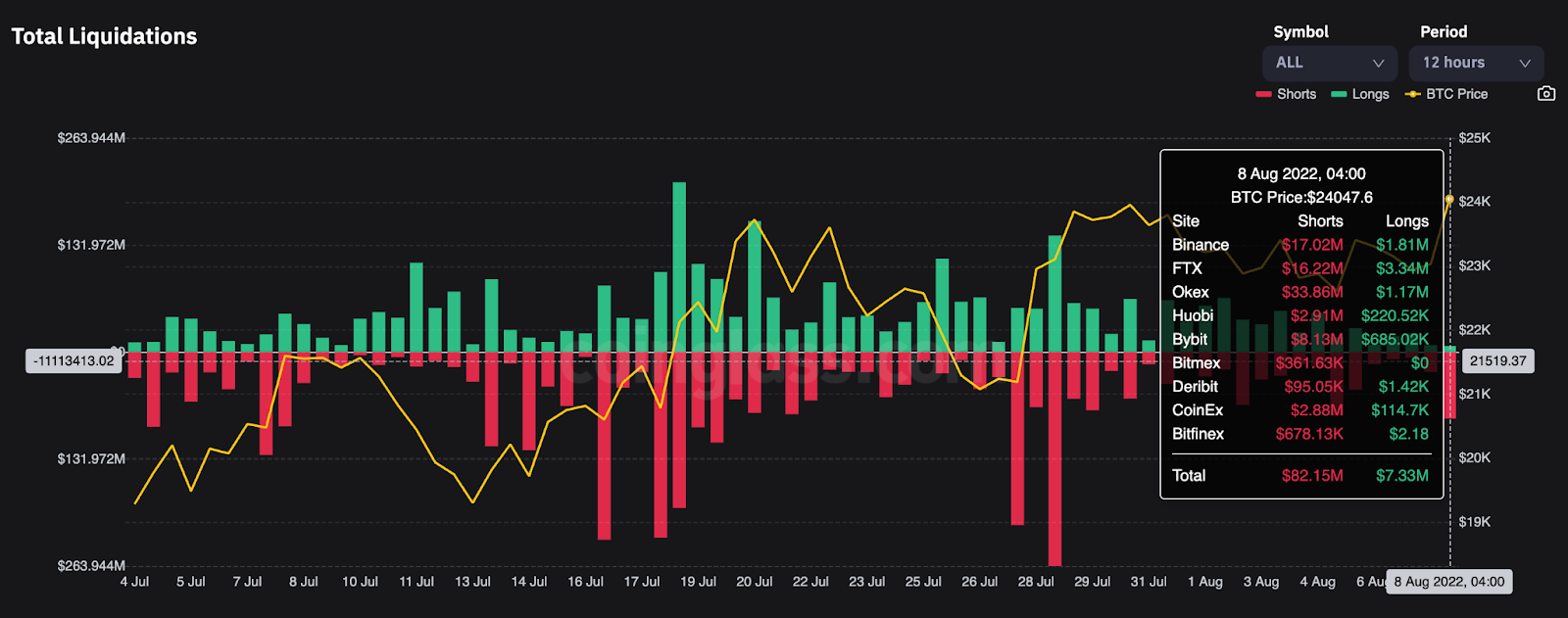

The lack of a clear price movement continues to keep the market in a state of uncertainty. As long as the news remained calm, liquidations did not exceed 20-30 million per day. A surge of volatility in Asian session at the beginning of this week and movement of ETN above 1800 USD led to a sharp increase in the size of closed positions. Leaders were Binance(19M USD), FTX(19.5M USD) and OKEX(35M USD).

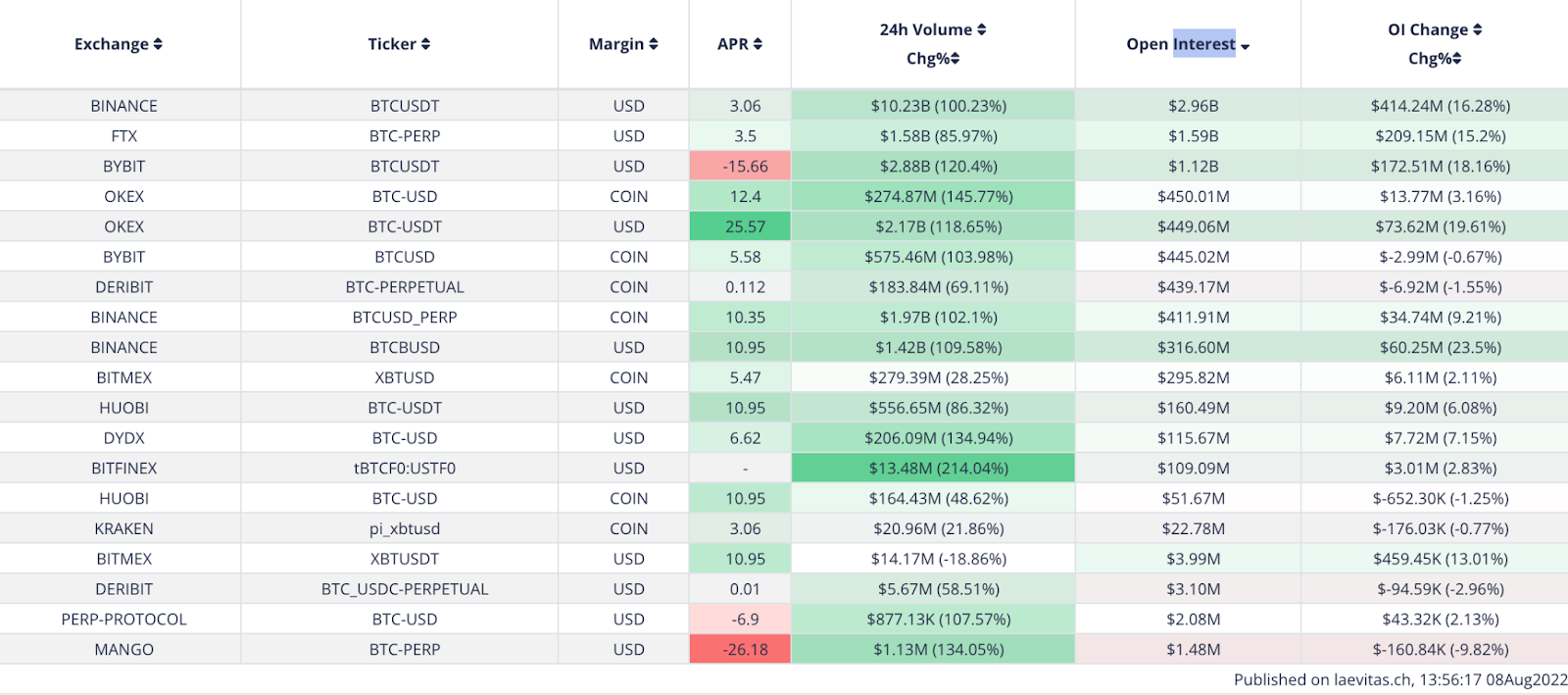

The situation in the market for funding margin positions continues to be volatile. Rate parameters vary widely across platforms and instruments. Thus, for BTC on perpetual swaps, arbitrage is still possible – BTC-USDT with settlement in dollars on OKX and BYBIT have diametrically opposite rates of 25% and -15% for trading volumes above USD 2bn. This inconsistency in the use of capital could indicate a significant bias in the assessment of the asset’s future price direction, and implies a weakness in current growth.

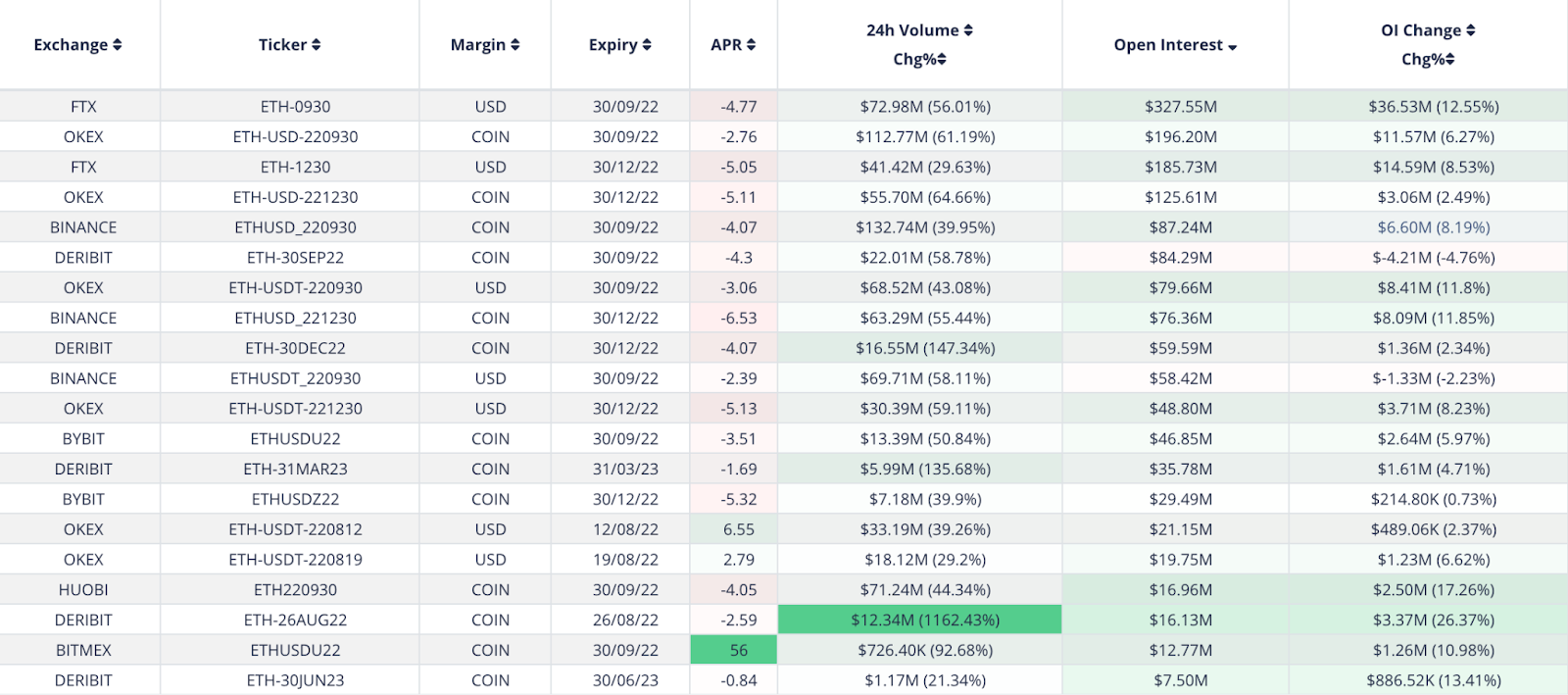

Additionally, it should be noted that most of the futures for ETH are negative. It seems that in this case derivatives are used as a balancing position as part of a complex strategy based on growth expectations and the purchase of spot or call options ahead of the expected move to the new consensus algorithm in September.

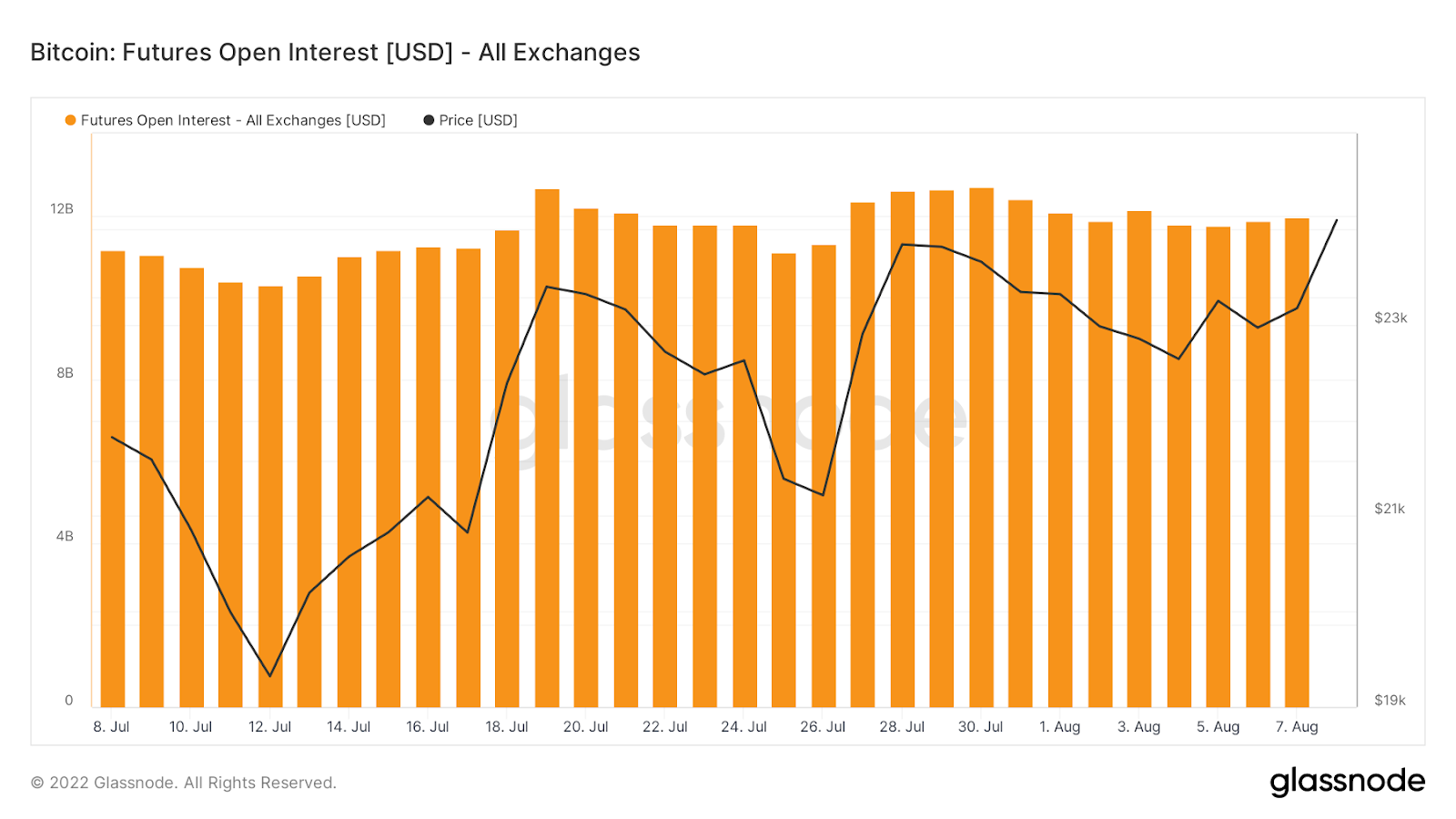

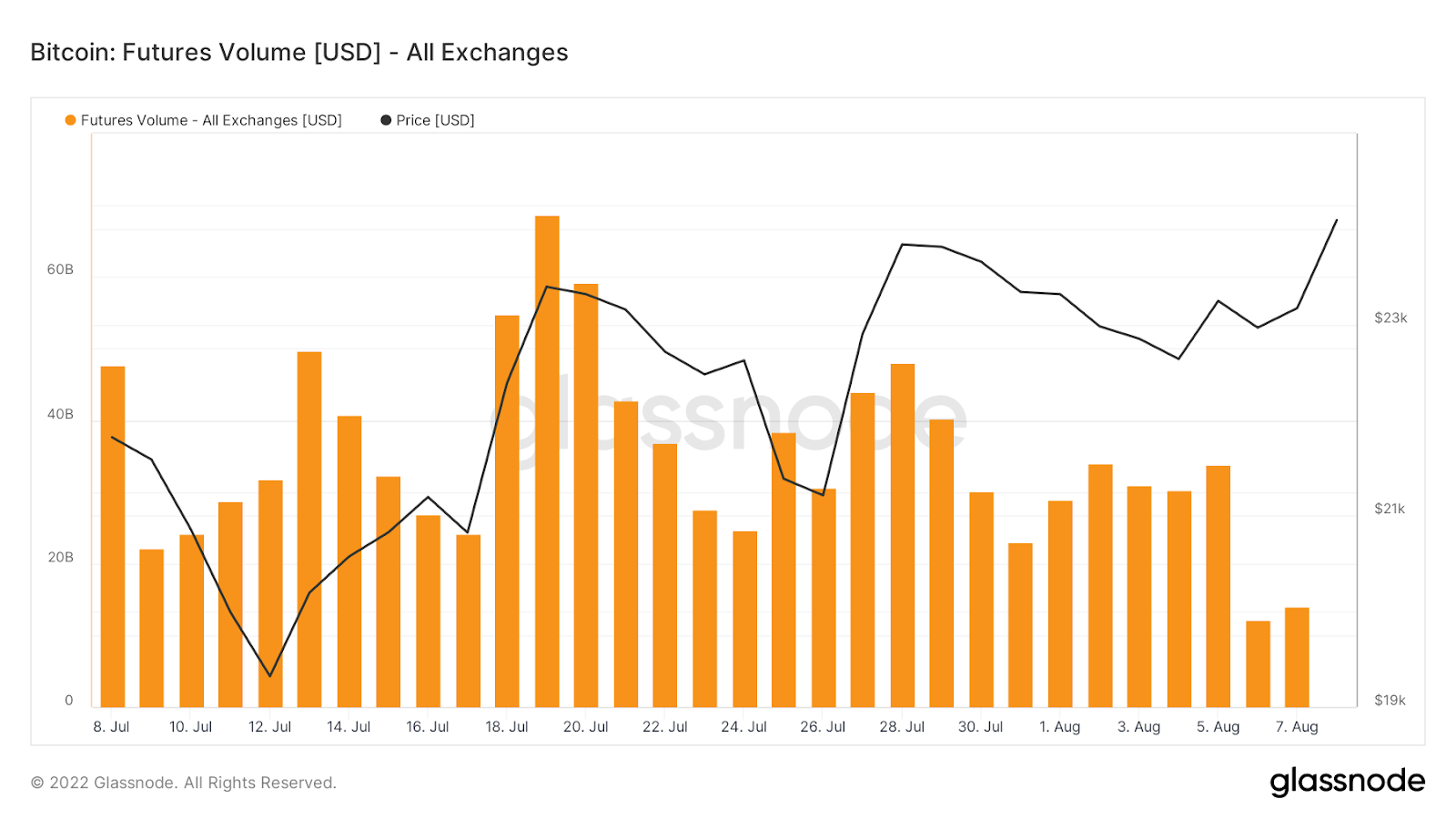

Despite a stable level of open interest in BTC futures trading (holding above the USD 12 billion mark) trading volume continues to decline, indicating weak liquidity in the market. A decline in trading activity in a rising spot market is often indicative of a weak market and an uncertain or short-term price movement.

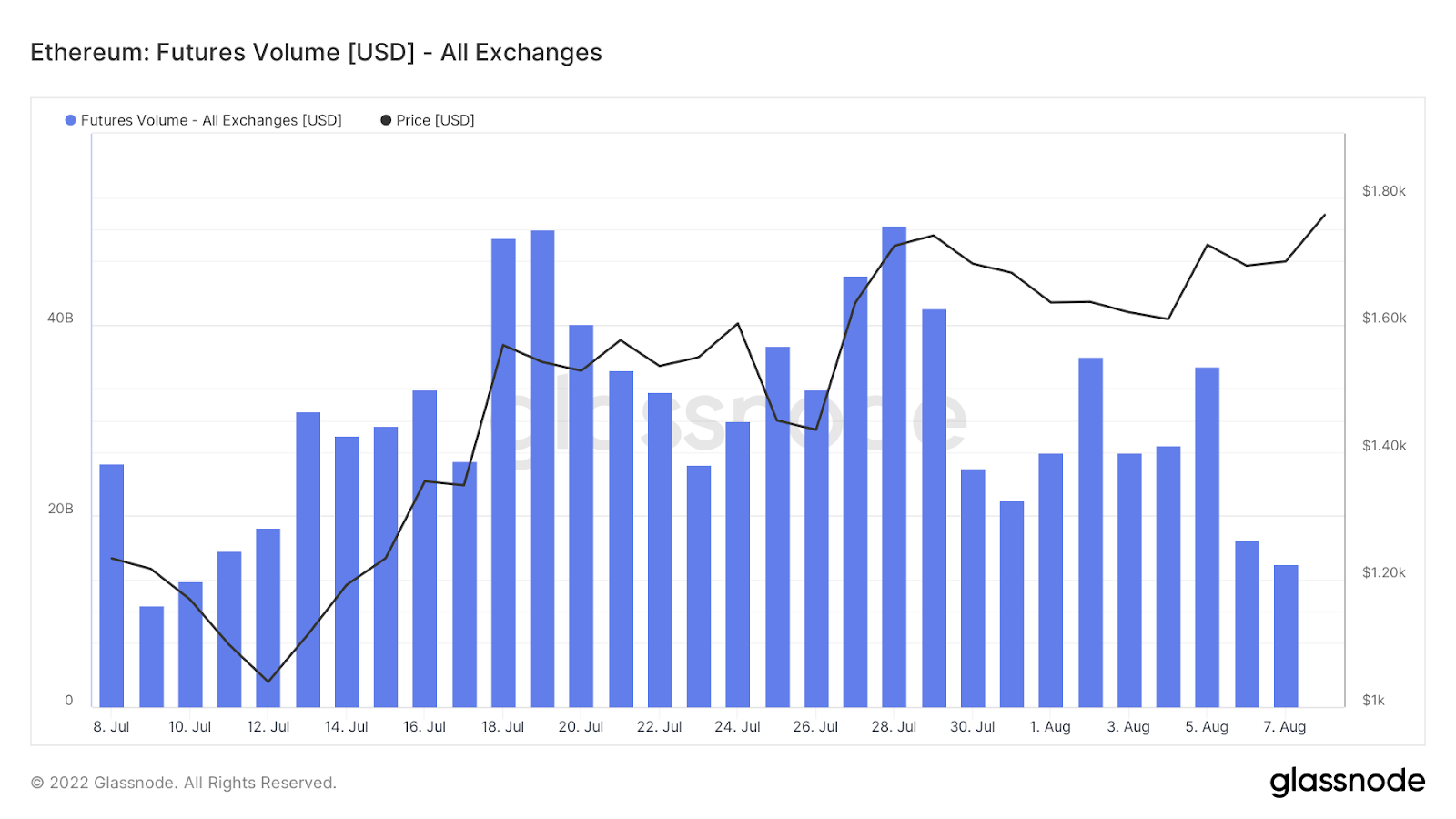

Against the backdrop of trading volume, the situation for Ethereum futures looks even more dramatic. The almost halving of figures from around USD 40 billion, as well as the downward trend over the past two weeks, could indicate a possible pause in the assessment of September blockchain prospects, as well as a lack of new directed liquidity in the market.

According to the oh-chain data from QryptoQuant analysts, the current price decline cycle has been an attractive period for concentrated investment in BTC by large holders. The levels of 20 000 and 30 000 were interesting enough for buybacks and can act as a benchmark for determining the likely minimum price in the current market cycle.

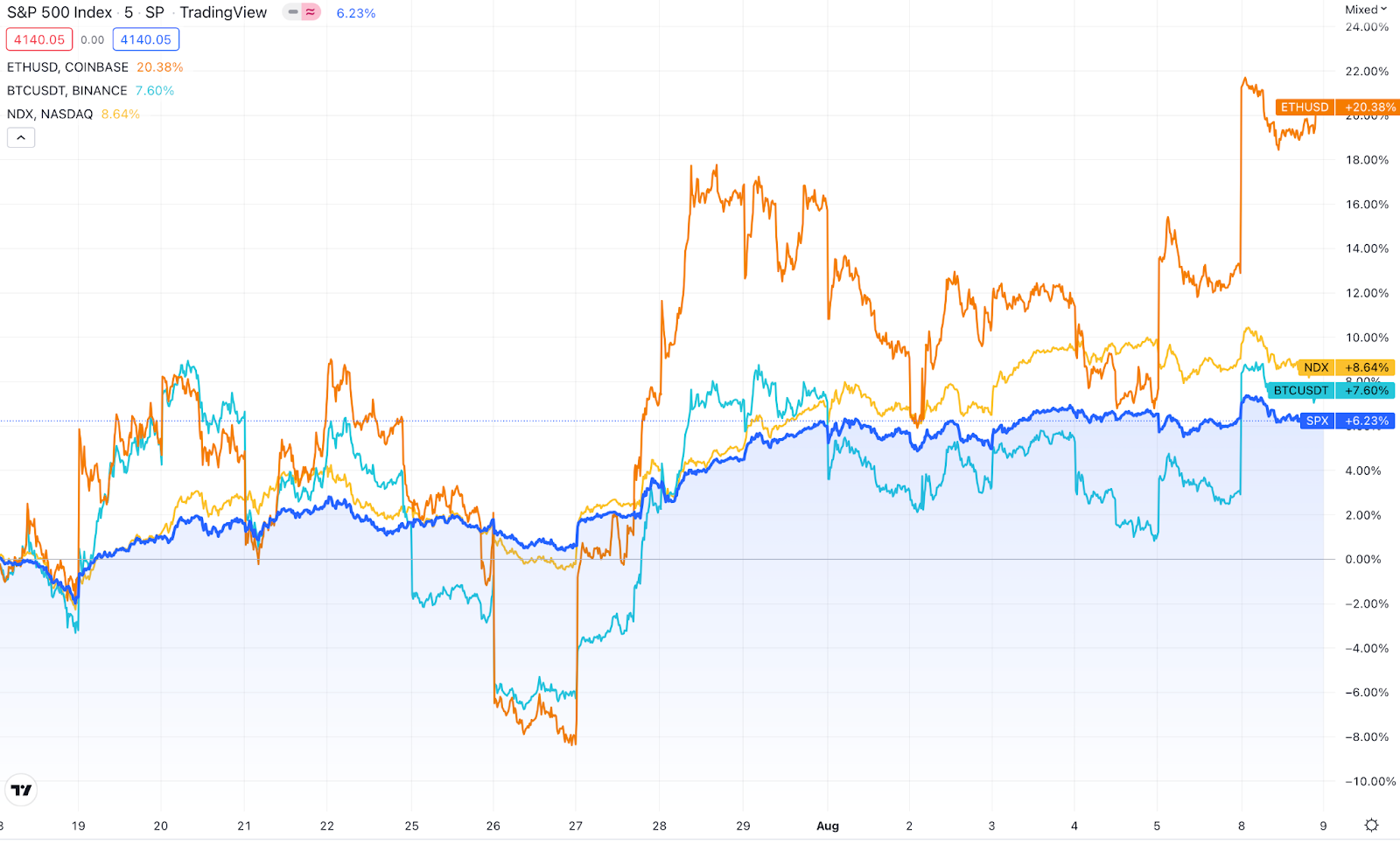

Over the past 20 days, Ether has shown a much stronger momentum, outperforming both the classic market indices – S&P500 and NASDAQ – as well as its main competitor BTC. Despite this success, the macroeconomic situation is slow to improve, which continues to weigh on the price of all assets in the crypto market. The US Federal Reserve, and the world’s major central banks following it, balancing high inflation and a recessionary economy is limiting the outlook for crypto asset prices. However, if the monetary authority’s decision is focused on economic growth and facilitates liquidity flows by opting to fight the recession, financial markets could come alive again and cryptocurrencies and technology stocks will be the main beneficiaries of these changes as well.

This overview was prepared by the analytics department of the Biqutex crypto derivatives exchange