The Derivatives Magazine #7

The lack of strong negative news, positive macro comments from the Federal Reserve and ECB heads and the ensuing correction in traditional markets provided significant support to the crypto asset market. Total capitalisation rose by 12% to around USD 950 billion with strong growth in altcoins (e.g. compound, uniswap, polygon up over 25%). The situation with 3 Arrows Capital continues to escalate in terms of the number of victims and the extent of the damage. For example, Voyager Digital reported the equivalent of $650 million in unpaid debt. However, judging by the lack of significant reaction on the market, news of this nature is already priced into the stock market.

According to Coinglass analytical service, liquidations have declined significantly, and we can conclude that the Bitcoin price is currently consolidating and remains weakly volatile in the short term. After last week’s staggering liquidations, this time the average daily amount did not exceed 100 million per day, which is three to four times less than a week earlier.

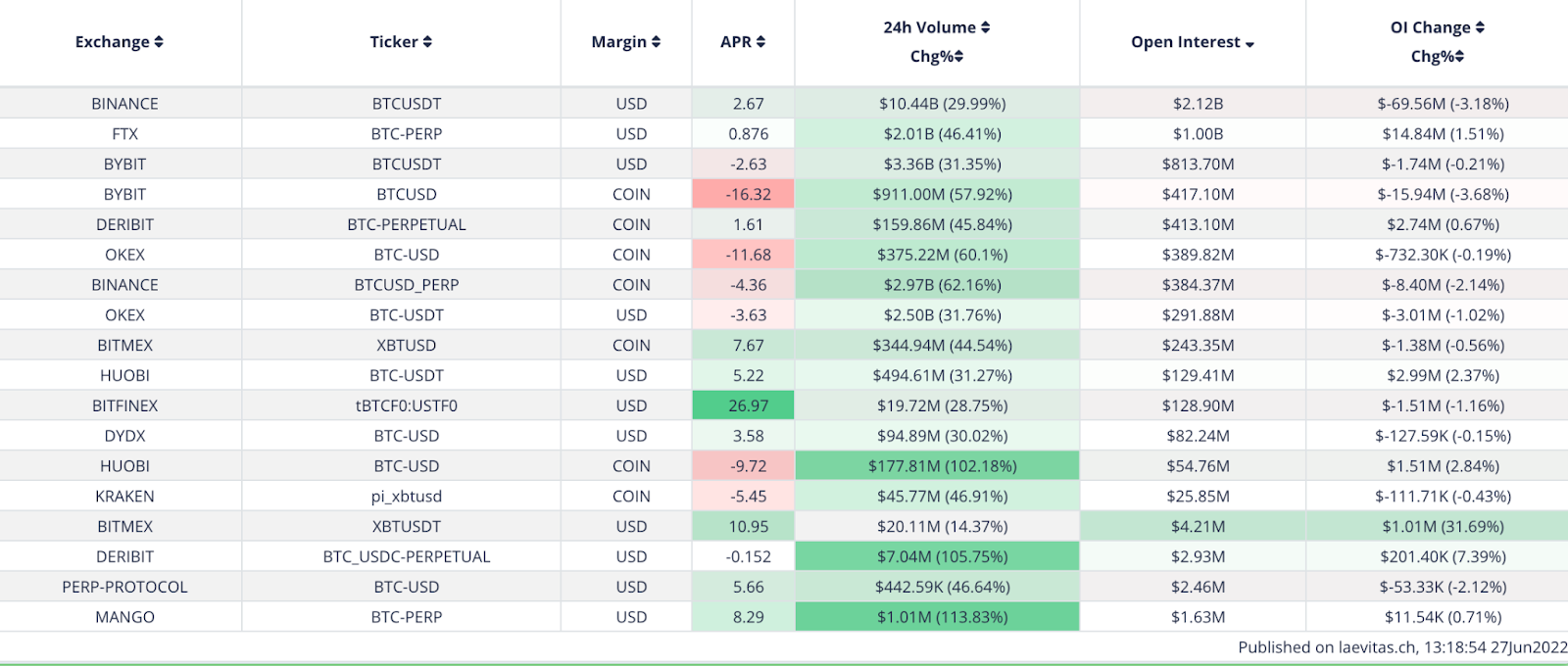

However, the reduction in overall volatility has not matched the consolidation of capital markets and cash flows on the exchanges. Funding rates for open-ended swaps are still rather fragmented, ranging between 2% and 26%. The largest volume of open interest (more than 1 billion) is concentrated on three exchanges – Binance, FTX, BYBIT.

After the June quarterly contracts expire, the bulk of interest traded for the September contracts. In the short term, traders do not use futures to build trading strategies, perhaps assuming that major market-moving events have already occurred.

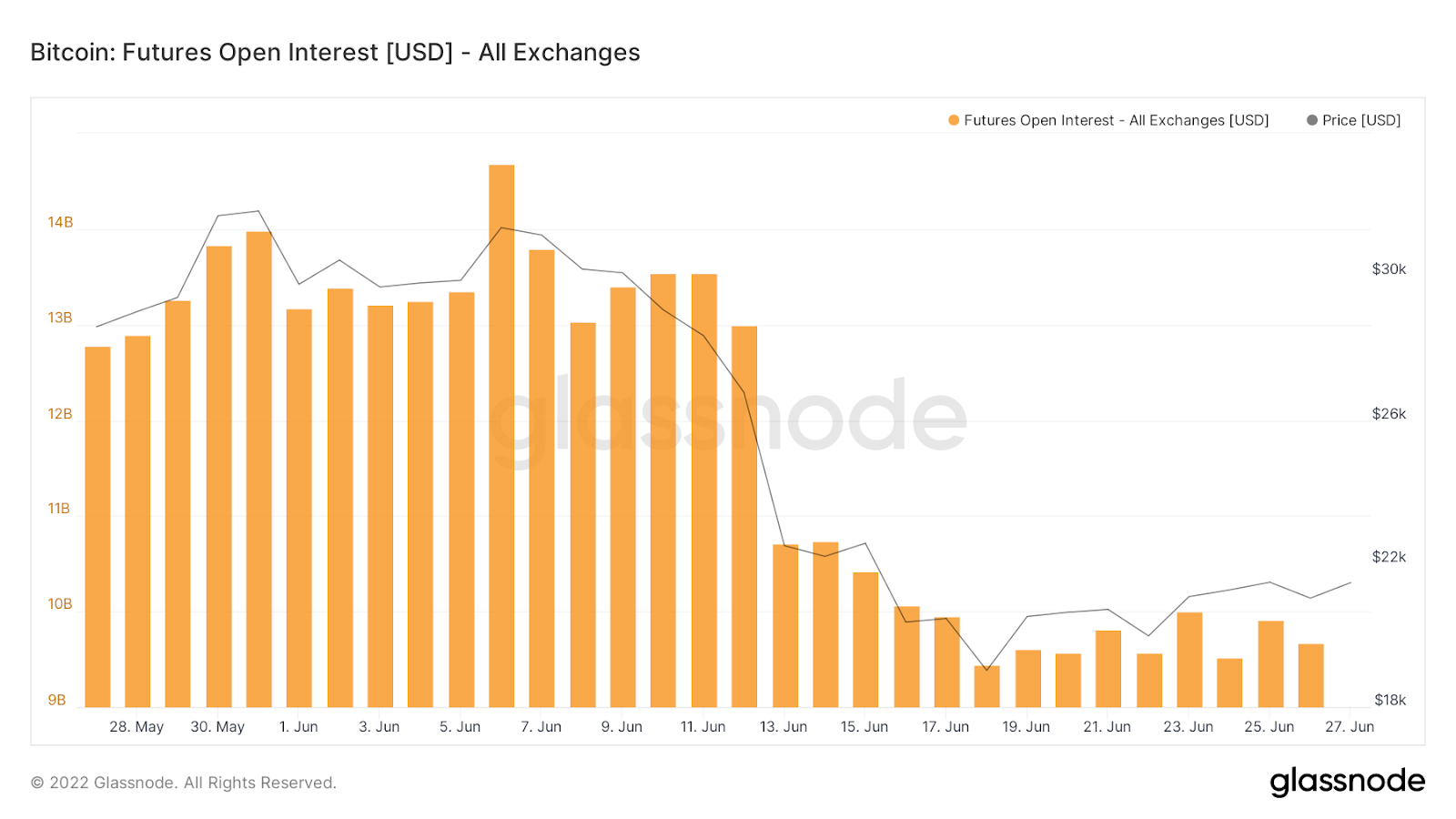

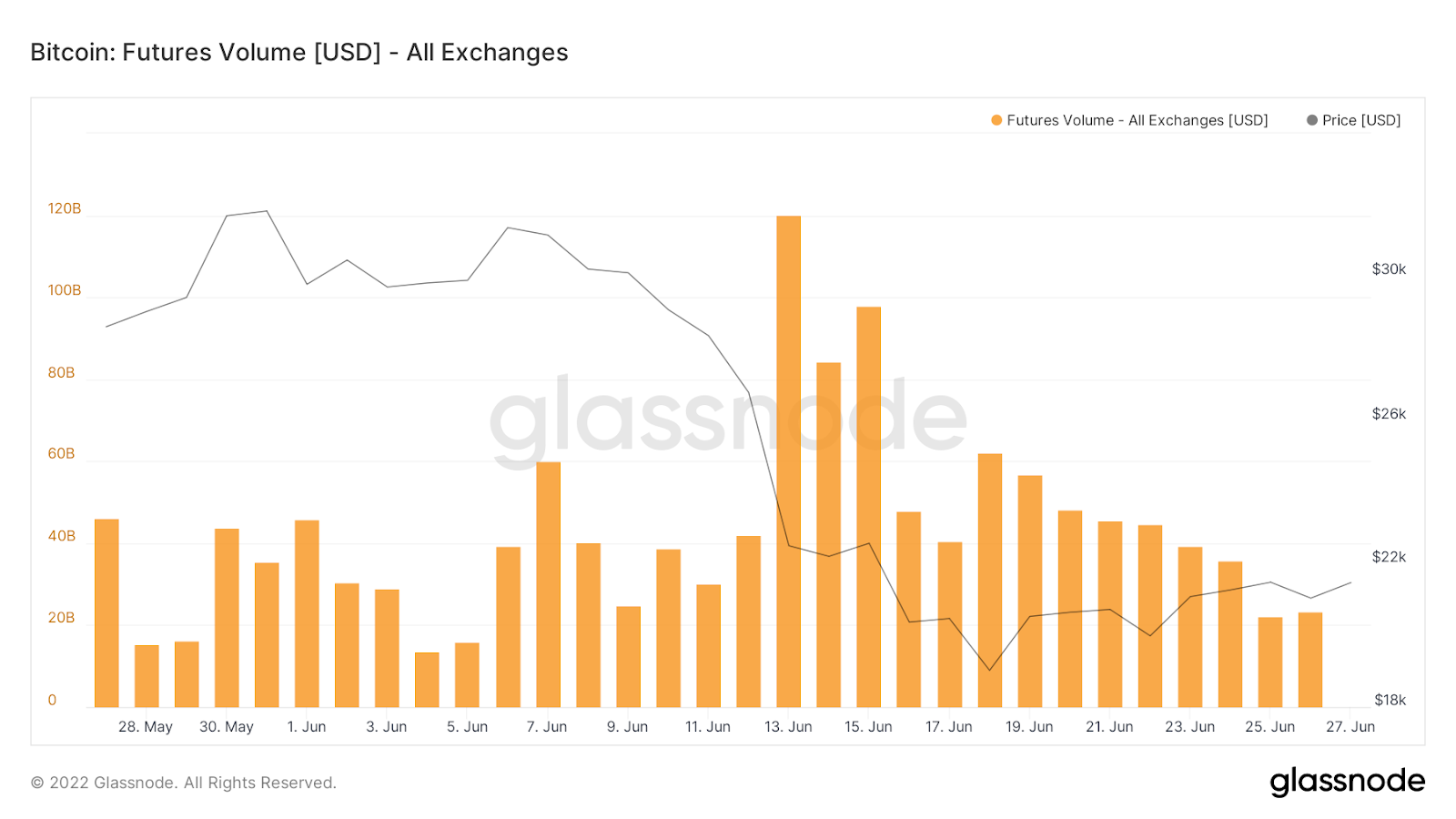

Total BTC futures trading activity has stabilised at around $20 billion per day, having roughly halved over the last decade. At the same time, the volume of open interest remains at the same level (around USD 9.5 billion), indicating the current short-term market consolidation.

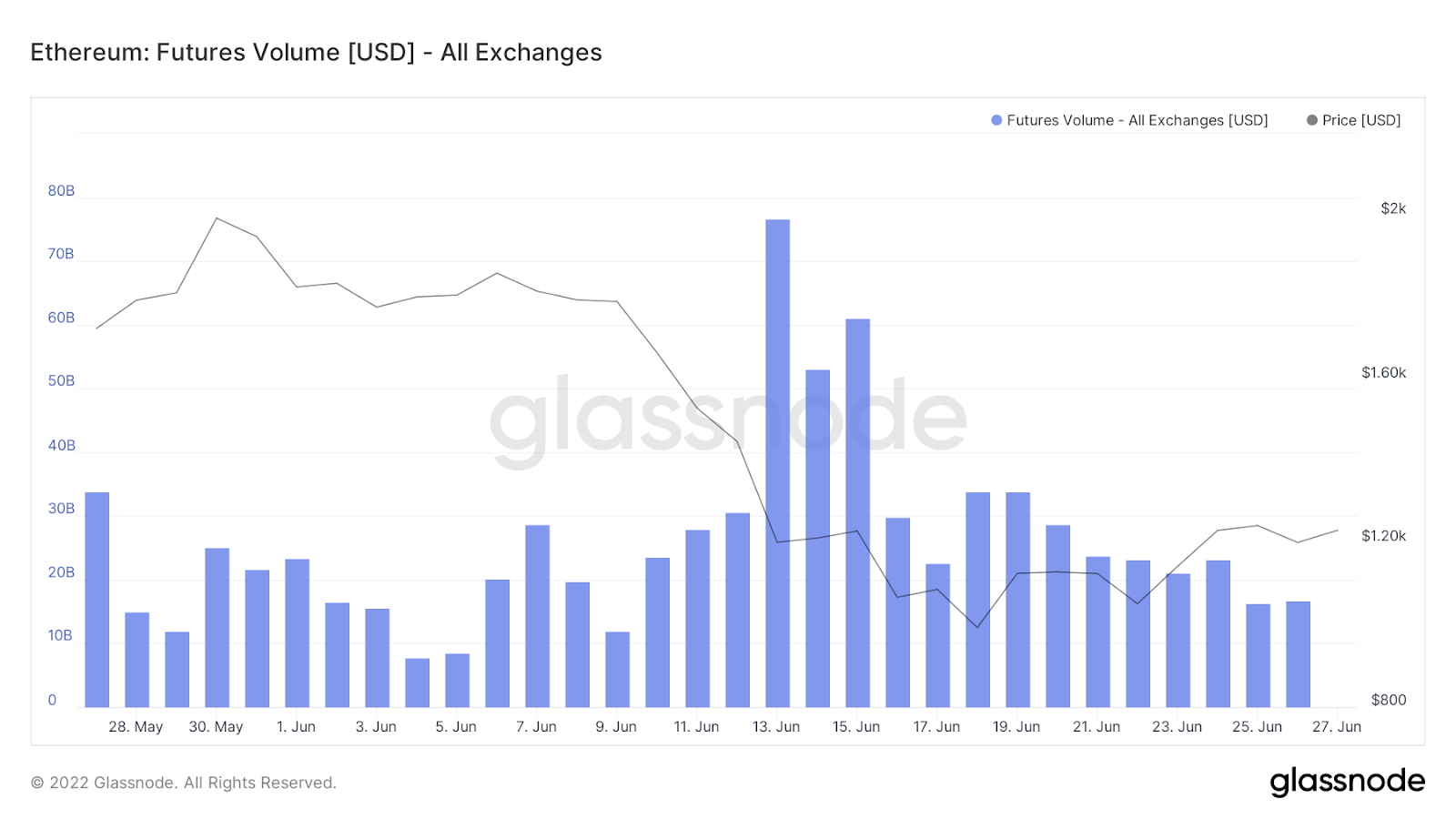

.The ETH trading dynamics continue to diverge from BTC. Despite the drop in trading volume to $10 billion a day, the level of open interest rose from lows to $4.7 billion, reflecting more optimism about the price in the medium term. The presence of a standalone news event (transition to the new PoS consensus algorithm) continues to have a positive effect on future valuations of Ethereum.

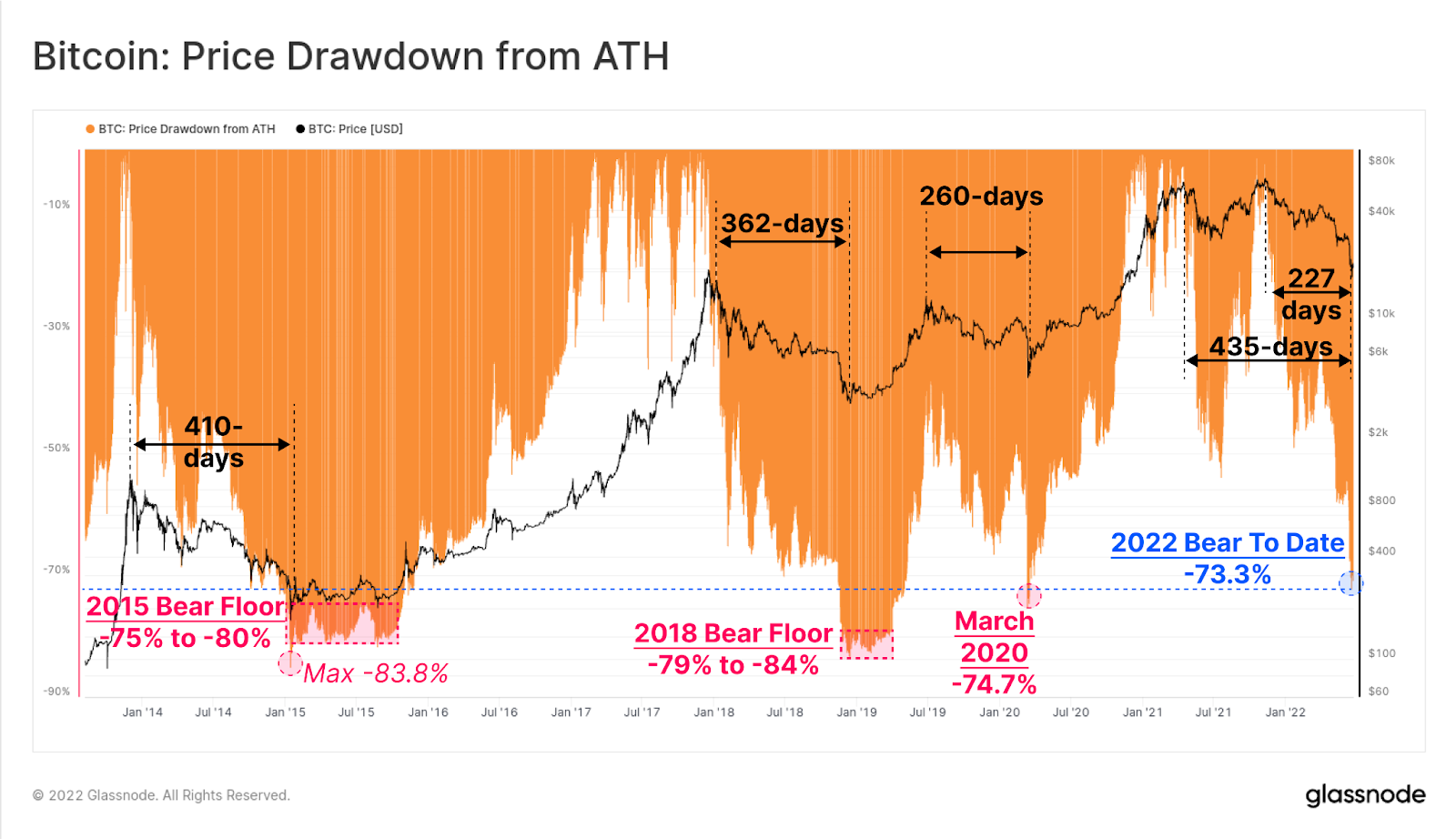

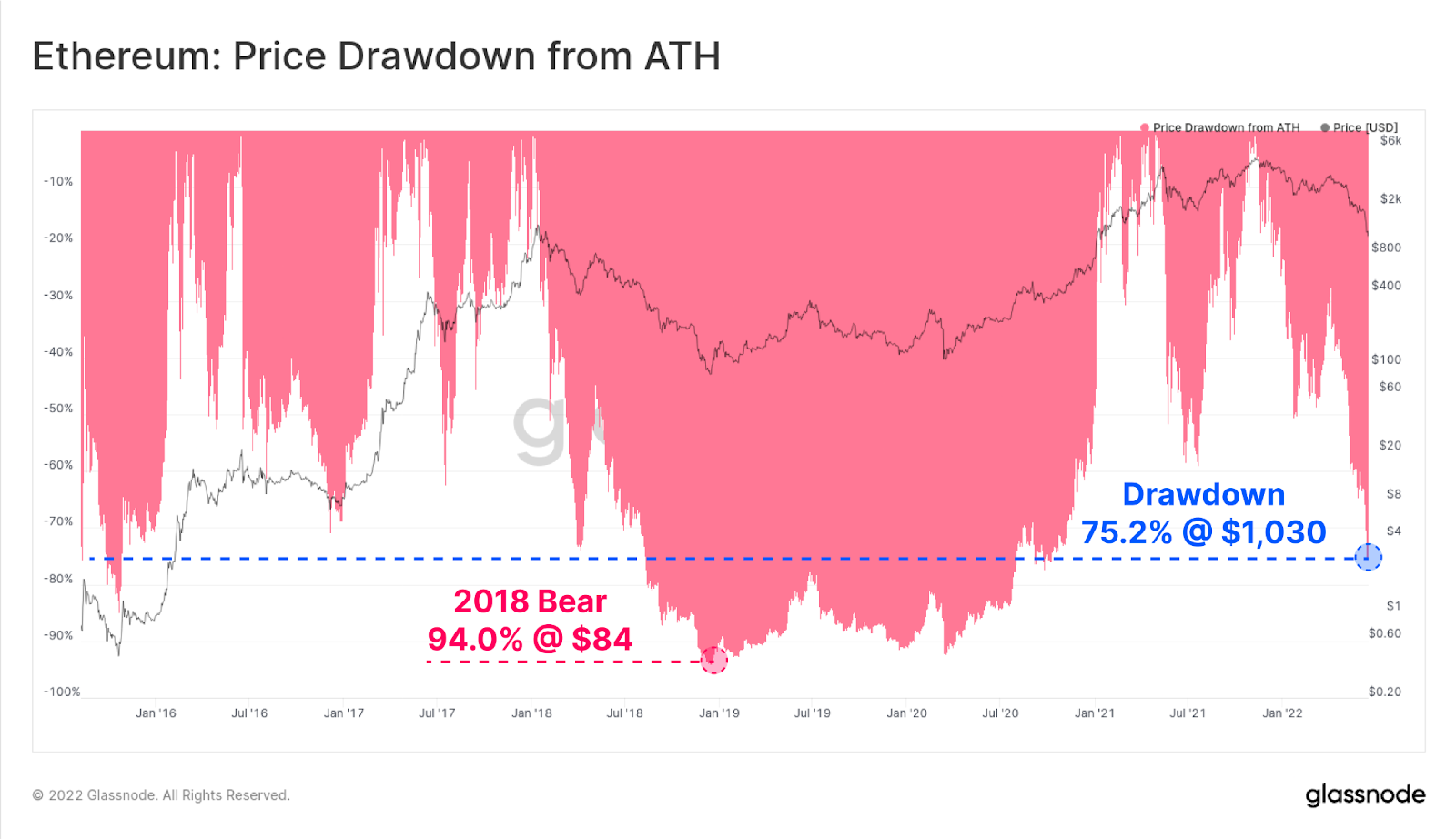

The drop in the value of BTC and ETH from their historical highs is approaching the peaks corresponding to past market cycles of price declines. Despite the magnitude of the drop (more than 70%), these types of declines have been in the markets before and usually coincided with a prolonged bear market. The current market situation significantly differs from past periods in terms of greater liquidity and number of participants, much greater penetration of cryptocurrencies into the daily information agenda and much more mature infrastructure. Recognition of the industry, primarily by investment companies and financial institutions, has allowed professional participants in the crypto market – such as miners, brokers and “neo-banks” – to access liquidity and instruments from traditional markets. As a consequence, the active use of collateral for crypto assets or mining equipment has greatly influenced the growth of the industry in 2020 and 2021. However, the use of loans has led to increased risks, most of which have materialized as the price has fallen over the past month. Bankruptcy of ecosystems (terra-luna), crypto investment companies and protocol hacks have led to a severe crisis for the industry. The current process of reassessing collateral values, collecting debts and sorting out cross-obligations is very painful for most market participants. Nevertheless, it is necessary for the industry to shake off excessive optimism and credit overhang and get through a turbulence period in global markets and a monetary policy tightening period with dignity. Per aspera ad astra – the ancient Latin wisdom is still relevant today. Especially now.

This overview was prepared by the analytics department of the Biqutex crypto derivatives exchange