Luna gambit for the crypto market

An entire blockchain ecosystem with over $30 billion in total funds raised was destroyed almost to the ground, causing huge losses for investors and nearly dragging the entire market down with it.

The news background and financial markets have been under constant pressure recently. Inflation, tightening monetary policy at major central banks, rising commodity prices (fuels, metals, products) and an increasingly real global recession leave little room for stock market optimism.

Such a global situation is certainly affecting the cryptocurrency market. Bitcoin has fallen for the seventh week in a row, which is the record high in trading history. The fall has particularly accelerated since May 5, amid the dramatic collapse of the Terra (Luna) ecosystem.

An entire blockchain ecosystem with over $30 billion in total funds raised was destroyed almost to the ground, causing huge losses for investors and nearly dragging the entire market down with it. Given the significance of the events surrounding this story, it makes sense to look more closely at what happened, as well as options for the future (both for risk insurance and extra returns).

So, how did the situation develop and where did it all start? To begin with, we should briefly describe the UST stableсoin mechanics, which was one of the foundations of the entire ecosystem. The basic balancing mechanism involved the ability for any blockchain user to exchange 1 LUNA token for a proportionate amount of UST at the market rate, with LUNA being burned. And vice versa. Accordingly, the higher the token is, the more stablecoins can be obtained.

In addition, one of the central depository protocols on Terra’s blockchain, Anchor, which accepted most of the free liquidity (at a maximum of about UST 12 billion), was set to a fixed yield rate of 20%. This rate required a large amount of new liquidity to pay out, and was set in anticipation of geometric growth in the number of blockchain users. The calculation paid off, but the quantity and quality of the Luna Foundation Guard special balancing exchange rate reserves could not keep up with the volume of funds raised. As a result, shortly before the major events of the rate crash, there was a situation where about $200 million had to be raised each month in order to pay the interest on Anchor deposits. This liquidity situation in place with the stablecoin balancing mechanism was quite volatile and put pressure on Terra’s blockchain. In order to balance the UST issue collateral and to diversify the reserves, the developers decided to add BTC, AVAX and some other tokens from the top 100 capitalisation ranking to the collateral. As a result, after accumulating more than 80 000 BTC on the LFG’s balance sheet, a situation that led to a drop in capitalisation and liquidation of over $2 billion worth of derivatives traders alone took place.

Before going any further into the process, it should be stressed that some of the information is currently unconfirmed and based on speculation and opinions of crypto industry experts. Collecting direct evidence and references is difficult because of the scale of the transactions, both in terms of the amount and the number of protocols, blockchains and trading tools involved.

One of the most detailed versions of the events is outlined in the Twitter threads of crypto enthusiasts – @OnChainWizard (version 1) and 4484 (version 2). If you summarise their reasoning, you get roughly the following picture:

1. A large trader (it is not currently known who the company is or whose trading desk it is) received 100 000 BTC (most likely via an OTC loan) and converted some funds into a LUNA token, which they sold on centralized exchanges to put pressure on the price.

2. In parallel with the operation of centralized exchanges, the Defi segment was involved – all the lending protocols in the various blockchains that supported the operation of the LUNA token borrowed all the free balances. The Venus protocol on the BNB chain is a case in point.

3. Another vector of the attack was the exchange pool on the Curve decentralized exchange, where UST was traded together with USDC and USDT in proportions of $170 million each. As a result of the attacker’s actions, all liquidity other than UST was withdrawn from the exchange pool.

4. All these actions took place against the backdrop of a general market decline and an information campaign to discredit Terra through Twitter bots.

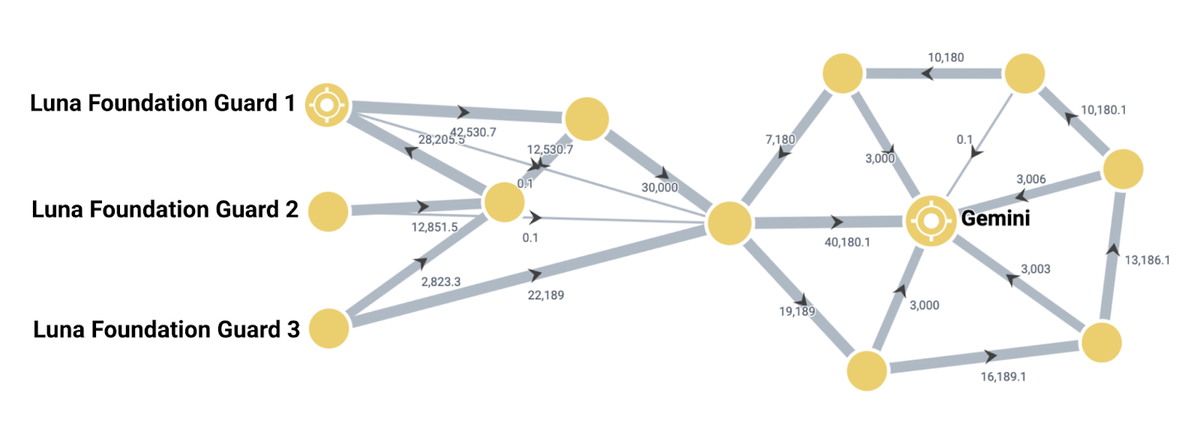

5. The LFG was forced to sell its reserves in BTC (withdrawal in three tranches to Binance and Gemini addresses – source 1, source 2) to restore the security of the stablecoin. In addition, the peg stabilization mechanism was designed to support around $150 million per day and fell short.

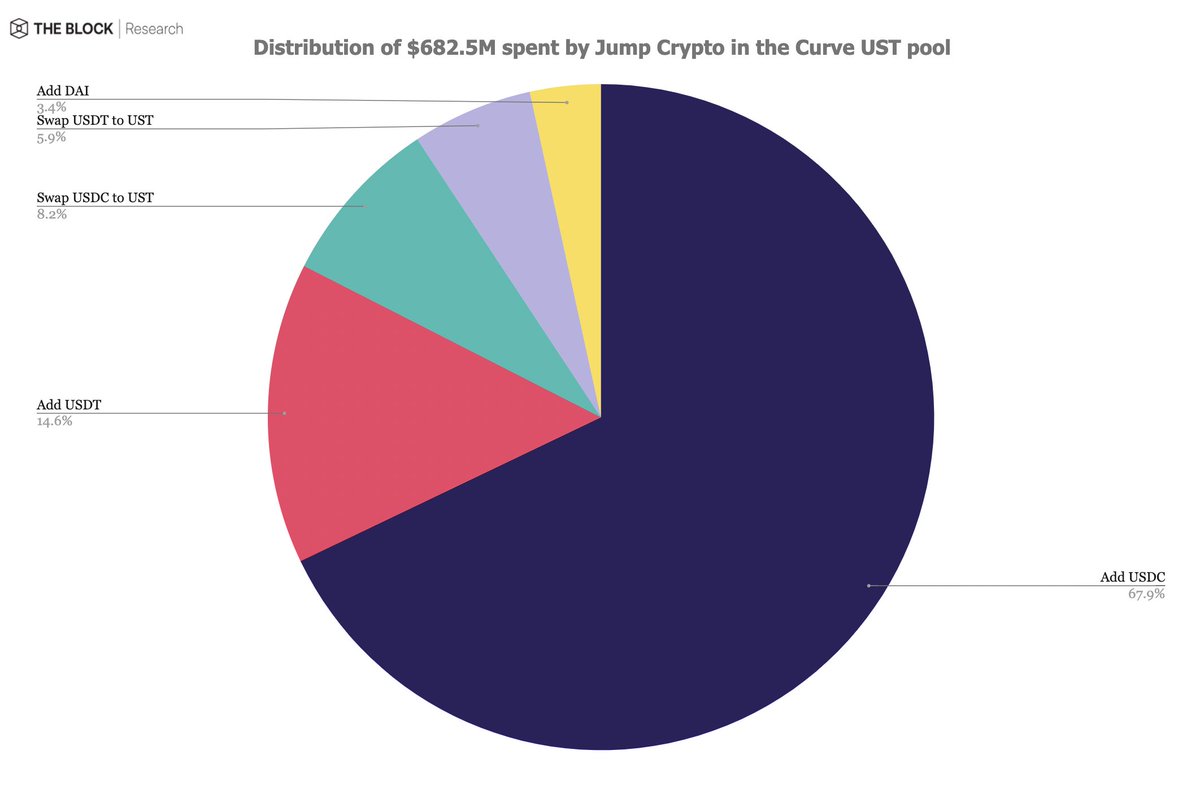

6. In addition to LFG, Jump Capital, a large cryptocurrency trading firm, was actively involved in defending the UST exchange rate peg. The company pulled reserves from Lido’s deficit-return protocol – stETH, as well as other assets to the tune of about 680 million, but even that was not enough.

7. As a result of a combination of stress factors — falling BTC collateral value (with a minimum at 26 000), pressure from the withdrawal of several billion USTs from the Anchor deposit protocol and their conversion into other stablecoins, constant price pressure on the LUNA native token and a 750x increase in issuance (due to a particular balancing mechanism), dispersion of liquidity across different blockchains – asset values collapsed by 99% and effectively the entire Terra ecosystem was in shambles.

Large investment funds such as Michael Novogratz’s Galaxy Digital, Binance and Delphi Digital suffered losses. In addition, numerous retail investors and blockchain users were affected. The size of the attack team’s profit is roughly estimated to be $800 million – but it is difficult to determine exactly due to the many decentralised platforms and centralized protocols that were involved. LFG currently retains assets with a book value of just over $20 million. Founder and CEO Do Kwon has launched a vote to create a new copy of the blockchain without launching a stablecoin.

The events surrounding the unbalance caused a lot of resonance in the press and among authorities in various countries. For example, Treasury Secretary Janet Yellen cited the UST example as one of the arguments in favour of faster cryptocurrency regulation in the US. South Korean lawmakers expressed a desire to personally talk to the Terra founder Do Kwon about potential fraud (due to non-transparent transfers and contradictory announcements, some MPs had the impression that some funds may have been withdrawn for personal gain).

Overall, these events have shown that game theory and subject motivation do not always work in reality at the same speed and to the same extent as on paper. Despite the large number of users and the organic foundation of the payment system, this was not enough to withstand an external financial attack.

What were the options available to the average trader to save or earn?

When investing in a volatile asset, there are several ways to generate returns – from value appreciation, from earning interest for providing collateral, from hedging positions.

Whereas the rise in value and interest rates are less dependent on the investor, the use of hedging instruments and the yield on them is entirely in the trader’s hands.

The main hedging method in this case could have been futures and options on the underlying asset (LUNA token) or on the UST Algorithmic Stablecoin. LUNA token perpetual futures offered by a large number of centralized exchanges, but stablecoin futures is a rare instrument and currently represented only on one exchange – FTX. By the way, the first liquidity spike associated with the deviation of the UST rate from the benchmark was registered on this exchange. The Biqutex team is developing a progressive and innovative derivatives trading platform which will offer, among other things, futures on a wide range of stablecoins.

This research was prepared by the analytics department of the Biqutex crypto derivatives exchange